From shipping cars to building them

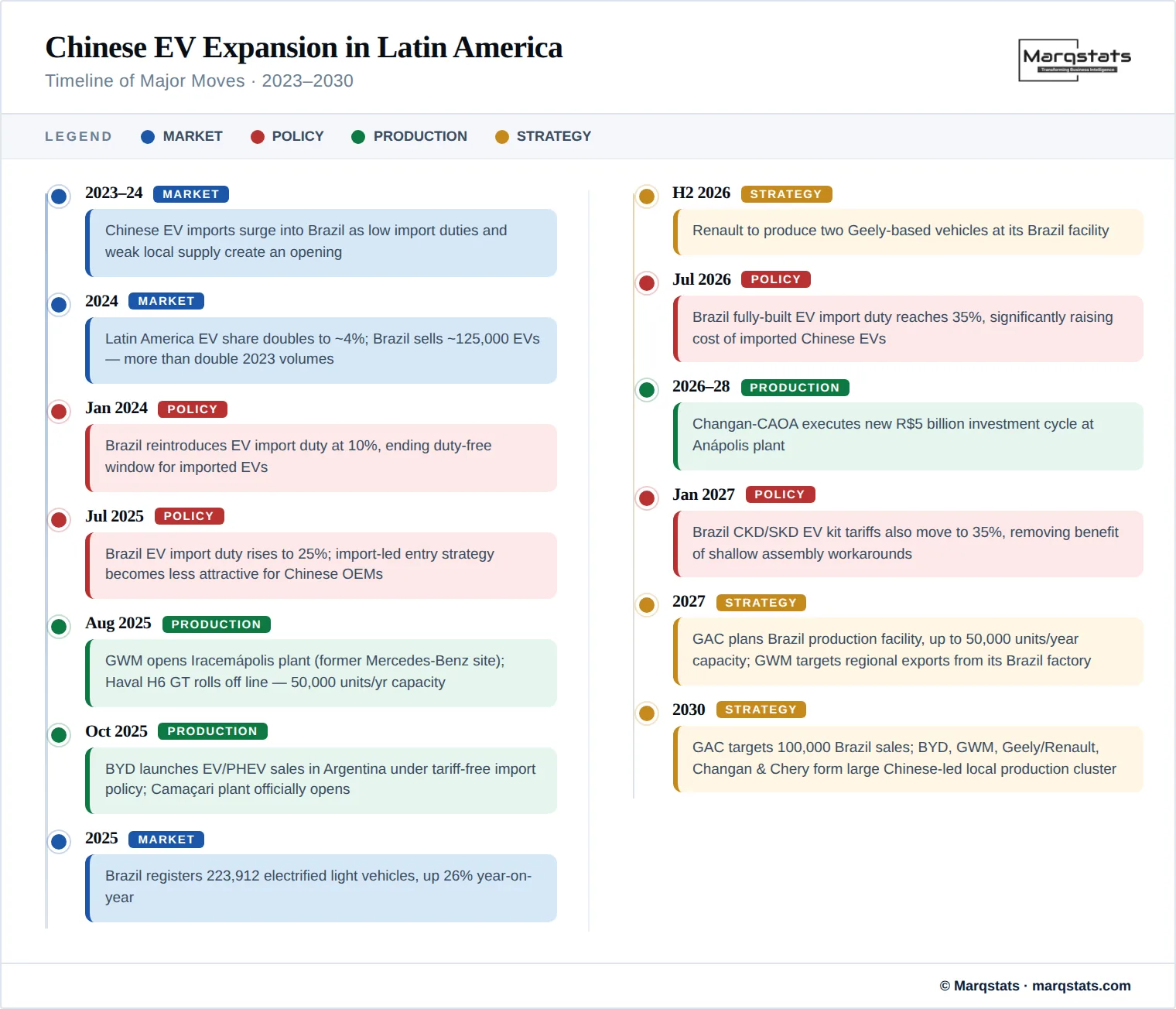

Chinese automakers have spent the last three years quietly rewriting their South America playbook. The early phase was import-led: ship affordable battery-electric and plug-in hybrid models out of Chinese ports, undercut legacy pricing, and capture electrified-segment share before Volkswagen, Stellantis, GM, Toyota and Hyundai responded. That phase worked. By 2025, Chinese-built vehicle imports into Brazil were running at roughly 200,000 units, equal to about 8% of Brazilian light-vehicle registrations.

The next phase is industrial. BYD, Great Wall Motor, Changan, GAC, Chery and the Geely–Renault partnership are all moving toward local assembly and progressively deeper localisation. The reason is structural — import tariffs are closing fast, labour and political pressure is rising, and the regional volume opportunity is large enough to justify factories rather than just dealer networks.

The pivot is not theoretical. Two plants are already running. Three more are funded. By 2030, South America's electrified-segment supply chain will include a meaningful Chinese-led production cluster anchored in Brazil and feeding the wider Mercosur region and the Pacific coast.

Chinese OEMs in South America are shifting from “China exports to the region” to “China designs, Brazil assembles, and the region absorbs locally adapted products.”

— Marqstats Analyst Team

Why Brazil is the pivot

Brazil is the only South American market large enough on its own to justify dedicated Chinese OEM manufacturing capacity. Total light-vehicle sales reached 2.69 million units in 2025, with around 2.19 million produced locally and roughly 498,000 imported. Brazil also produced about 2.65 million vehicles in the same year, exporting roughly 528,000 of them — mostly to Argentina, Chile and Colombia. That makes the country both a demand market and a regional export platform.

Electrification is moving faster than the headline market. Brazil registered around 224,000 electrified light vehicles in 2025, up roughly 26% year on year. The electrified share of total light-vehicle sales reached 9% for the year and touched 13% in December — the highest monthly share recorded. Within electrified sales, plug-in hybrids accounted for around 45% and battery-electric vehicles for around 36%. That mix aligns closely with the Chinese OEM product portfolio, which is strong in both PHEVs and BEVs.

Tariff policy is the forcing function. Brazil's electric-vehicle import duty has stepped up from 10% in early 2024 to 25% by mid-2025, and is scheduled to reach 35% in July 2026. Knock-down kit duties — long the loophole for shallow assembly — move to 35% in January 2027. Importing fully built vehicles from China will no longer be the cheapest way to serve the market, and shallow SKD assembly will not be a workaround for much longer.

The Brazilian production map

The Brazilian production footprint is no longer aspirational. It is being built.

BYD — Camaçari, Bahia

BYD has taken over a former Ford industrial site in Bahia, an investment that is symbolic as much as commercial. Initial capacity is 150,000 vehicles per year, with phase-two expansion planned toward 300,000. Operations launched on a semi-knocked-down basis and will progressively deepen to include stamping, welding, painting and a higher share of Brazilian-sourced components. The plant is also intended as a regional export base, with early units earmarked for Argentina and Mexico. BYD has separately announced a research and development centre in Rio de Janeiro, with completion targeted for 2028.

Great Wall Motor — Iracemápolis, São Paulo

GWM opened its Brazil plant in August 2025, taking over a former Mercedes-Benz site. The Haval H6 GT was the first locally built model. Capacity is set to scale from 20,000 to 50,000 units per year, with the Haval H9 SUV and the Poer P30 pickup added to the local lineup. GWM has signalled an intent to begin regional exports from the plant by 2027, leveraging Brazilian trade agreements with Mercosur, Chile and Mexico.

Changan with CAOA — Anápolis, Goiás

Changan's local production line, run in partnership with the CAOA distribution group, started in early 2026. Total committed investment in Anápolis stands at around R$8 billion, with annual capacity at 90,000 units. The strategic detail that matters most is product mix: Changan is localising flex-fuel and hybrid variants, not just battery-electric models. That recognises a Brazil-specific reality — the country runs on sugarcane ethanol, and a pure BEV strategy leaves volume on the table.

GAC — planned for 2027

GAC has announced Brazilian production from 2027, with capacity of up to 50,000 units per year and committed investment of around USD 1.3 billion through 2030. The brand is targeting 100,000 Brazilian sales by 2030, signalling that the second wave of Chinese entrants intends to compete at scale rather than at the margins.

Geely with Renault — São José dos Pinhais

The Renault–Geely partnership uses a different localisation route: produce two Geely-based vehicles at Renault's existing Ayrton Senna plant from the second half of 2026, with a planned R$3.8 billion investment programme and a new zero-emission Renault model on a Geely architecture in 2027. For Geely, this is the lowest-risk path to local content. For Renault, it is a way to refresh its Brazilian portfolio without rebuilding capability from scratch.

Chery, Stellantis-aligned plays and Leapmotor

Chery already has a long-standing local presence through CAOA's Anápolis plant, where Tiggo 5X, Tiggo 7 and Tiggo 8 variants — including hybrids — are built. The Omoda and Jaecoo brands are preparing a Brazilian footprint. Leapmotor, separately, plans to build C10 and C10 REEV models inside the Stellantis FCA Brasil plant in Pernambuco, leveraging its global tie-up with Stellantis.

Beyond Brazil — the demand pull

The localisation story sits inside Brazil. The demand story spans the continent — and it is moving faster than legacy OEM responses.

Chile — already mainstream

Chinese brands reached around 30% of new passenger car sales in Chile through early 2025, and Chinese-origin vehicles accounted for over 38% of total vehicles sold by manufacturing origin year-to-date by April 2025. This is not a pure EV story. It spans SUVs, pickups, commercial vehicles and mass-market sedans. Chile's open-market trade regime and absence of a domestic auto industry make it the cleanest test of pure brand competitiveness — and Chinese OEMs are passing it.

Peru — logistics leverage via Chancay

The newly opened Chinese-built Port of Chancay is materially shortening trans-Pacific shipping times and is being used as a re-export node to Chile, Ecuador and Colombia. Peru's hybrid and EV sales rose around 44% year on year in the first nine months of 2025 to over 7,000 units. Chinese EV pricing in Peru sits at roughly 60% of equivalent premium imports — a value gap that established premium brands have not been able to close.

Uruguay — early BEV mainstreaming

Chinese market share in Uruguay has more than doubled since 2023 to roughly 22%, with BYD now ranked the country's third-largest vehicle seller across all powertrains. Uruguay shows how quickly a Chinese OEM can move from EV-segment leader to overall top-three brand once the dealer network and aftersales backbone catches up.

Colombia and Ecuador

Both markets show a similar pattern. Chinese brands dominate the early electrified segment before legacy OEMs respond. In Ecuador, hybrids and EVs reached approximately 22% of the car market in early 2026, with BYD leading individual brand sales and 15 Chinese brands sitting inside the top 21 EV sellers.

Argentina — policy-dependent

Argentina remains the structural outlier. Total electric-car sales were under 500 units across most of 2025, but the country has opened a tariff-free quota of up to 50,000 electric and hybrid vehicles for 2026. BYD launched its first three nameplates in October 2025 with sub-USD 16,000 pricing at origin and a quota allocation of around 7,800 units. The mid-term picture is unclear — tariff-free access creates a real entry window, but Mercosur economics still favour OEMs with regional production.

What is actually different

Three things separate the current Chinese OEM South America strategy from the import-led wave of 2022–2024.

Product strategy is no longer EV-only

Chinese OEMs entering Brazil are deliberately localising plug-in hybrids, conventional hybrids and flex-fuel variants alongside battery-electric models. The Brazilian fuel-type mix in 2025 still showed flex-fuel vehicles at roughly 1.9 million units, or about 74% of total light-vehicle sales. A pure BEV play ignores three-quarters of the market. Changan's Anápolis flex-fuel localisation, GWM's pickup and SUV emphasis, and BYD's PHEV-led Brazilian launch sequence all reflect this lesson.

Localisation depth varies sharply

BYD started SKD and is moving toward fuller manufacturing. GWM is running a deeper assembly footprint from day one. Changan-CAOA is investing in flex-fuel powertrain localisation. Renault-Geely is using an existing facility. GAC has not yet started. Investors and supply-chain partners cannot treat these moves as equivalent — local-content trajectories will diverge meaningfully by 2028, and that will determine which Chinese OEMs are exposed when Brazilian content rules tighten further.

The policy backdrop has tightened

Brazil's tariff schedule effectively closes the import-led arbitrage window by July 2026 for finished vehicles and January 2027 for kits. Argentina's 2026 quota offers a temporary tariff-free entry but does not constitute a long-run industrial policy. South America's Chinese OEM landscape is therefore being shaped less by free-market economics and more by national tariff calendars. What has not changed is the demand pull — Chinese brands continue to win on price-to-feature ratio, and legacy OEMs in the region have not yet responded with comparable affordable BEV or PHEV portfolios.

Related reportASEAN Electric Vehicle Market Report 2026–2030The 2030 picture

Looking five years out, the most likely structure is the following.

Brazil becomes the Chinese OEM manufacturing hub for the region, producing electric vehicles, plug-in hybrids, hybrids, flex-fuel hybrids, SUVs and pickups, and exporting a meaningful share to Argentina, Chile, Colombia and beyond. Chile retains high Chinese import penetration and acts as the open-market benchmark. Peru continues as a logistics and distribution node via Chancay. Colombia and Ecuador see Chinese brands dominate the electrified segment as it scales. Uruguay confirms early BEV maturity with BYD as a top-three brand across all powertrains. Argentina's outcome remains policy-dependent — a meaningful Chinese OEM presence is possible but conditional on Mercosur-aligned local production decisions later in the decade.

Legacy OEMs will not be displaced. Stellantis, Volkswagen Group, GM, Hyundai-Kia, Toyota, Renault, Honda and Nissan together still account for the bulk of South American volume, and their flex-fuel ICE base in Brazil alone protects a deep revenue pool. What will change is the electrified, hybrid, compact SUV and value-priced segments — and that is precisely where industry growth is concentrated.

Bottom line

The headline shift in South America is not that Chinese brands are arriving — they have arrived. The shift is that Chinese OEMs are starting to industrialise their regional presence. Brazil is the pivot, with BYD, Great Wall Motor, Changan, GAC, Chery, the Geely–Renault partnership and Leapmotor either already producing or committed to producing locally. Other South American markets continue to provide the demand pull — Chile shows mainstream acceptance, Peru offers logistics leverage, Uruguay demonstrates how quickly a Chinese brand can become a top-three player, and Colombia and Ecuador confirm electrified-segment leadership.

The biggest structural change by 2030 will be that South America's electrified-vehicle supply will not come only from Chinese ports. A growing share will come from Chinese-owned or Chinese-partnered production inside Brazil — locally adapted to flex-fuel, ethanol, hybrid logic and regional consumer preferences, and exported across Mercosur and the Pacific coast. That is a different competitive problem for legacy OEMs than the import wave of 2022–2024, and it requires a different response.

─── END OF INSIGHT ───