A new supplier wave is forming

Thailand’s automotive supplier base is being rebuilt one component at a time. For thirty years the country’s parts ecosystem was designed around Japanese ICE platforms — one-tonne pickups, naturally aspirated engines, conventional transmissions, exhaust and fuel systems, stamped metal, rubber, seats and interiors. That ecosystem is still the largest part of Thai auto manufacturing. But it is no longer where the new investment is going.

In 2025, BOI auto-related approvals included roughly 200 companies, of which around half were Chinese-affiliated, including joint ventures. The list spans the full EV supply chain: lithium-ion battery cells, battery management systems, thermal management modules, electric powertrain components, traction motors, chargers, charging stations, electric two-wheelers and battery-swapping infrastructure. The pattern is clear. Chinese OEMs arrived first. Chinese parts suppliers are now following them in.

This is the third stage of the same shift. Stage one was Chinese EV imports into Thailand. Stage two was Chinese OEM assembly inside the country. Stage three — now visible — is supplier localisation. It changes the structural question facing Thailand’s legacy Tier-1s and SME network.

Thailand’s EV supply chain is shifting from “Chinese OEMs assemble locally” to “Chinese OEMs and their suppliers manufacture locally.” That is a different industrial outcome.

— Marqstats Analyst Team

Why suppliers are following the OEMs in

Three forces are pulling Chinese parts suppliers into Thailand at the same time.

Chinese OEMs already control the EV segment

Chinese brands account for over 70% of Thailand’s electric-vehicle sales. BYD, Great Wall Motor, Changan, GAC AION, SAIC-MG, Chery, Neta and Geely-aligned brands are now the visible face of EV retail in Thailand. Chinese OEMs collectively committed more than USD 4 billion under Thailand’s EV incentive structure, with BYD, GWM, Changan and GAC AION alone accounting for around USD 3 billion. When OEMs of that scale localise production, their suppliers come with them — it is faster, cheaper and more reliable than re-qualifying local Tier-1s on existing Chinese platforms.

BOI rules require deep localisation, not just assembly

Thailand’s 2025 BOI investment framework makes the supplier logic explicit. Battery-electric and BEV-platform projects must produce battery modules or packs within three years of starting EV production. At least one of three key parts — traction motor, battery management system, or driving and motor control unit — must also be manufactured locally within the same window. Additional incentives apply when more key parts are localised. This is no longer a vehicle-assembly policy. It is a supply-chain policy, and it forces upstream investment regardless of where each supplier originally planned to manufacture.

Production obligations turn imports into local sourcing

Earlier EV-import subsidies came with production commitments. Carmakers had to match imports with local output by 2024 and produce 1.5 vehicles locally for every imported vehicle by 2025. Exported EVs can now count toward those obligations, which has shifted Thailand’s supplier role from “domestic-only” to “domestic plus ASEAN export” — a much larger and more durable demand pool for component makers.

The supplier map, by component

Localisation is not happening evenly across the supply chain. Some categories are already at scale; others are early. Six clusters are worth watching.

Batteries — the leading edge

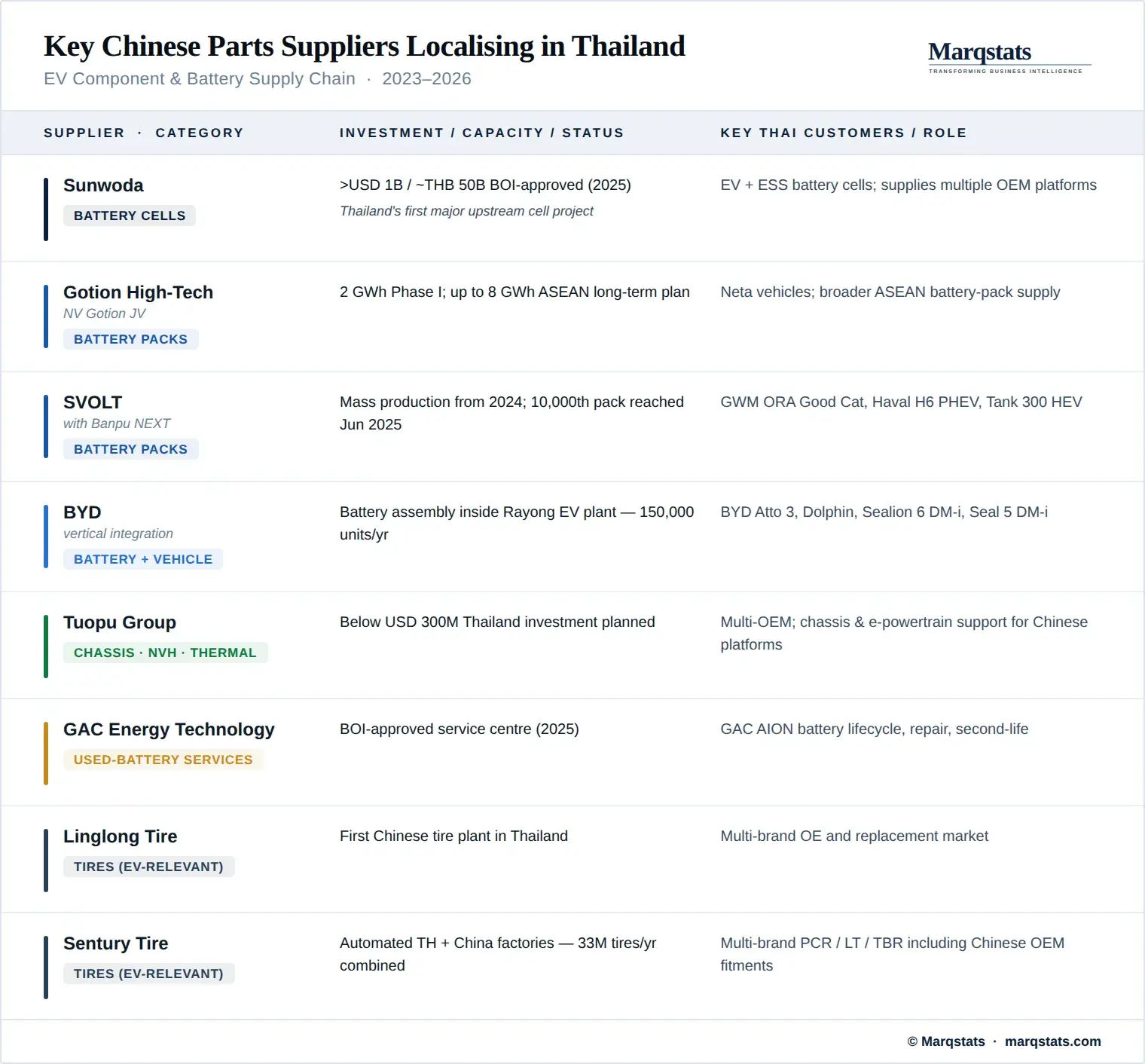

Battery localisation is the most advanced part of the Chinese supplier wave in Thailand. Three names define the current state. Sunwoda received BOI approval for a battery-cell project of more than USD 1 billion, reported at around THB 50 billion with 4,000 jobs — Thailand’s first major upstream cell investment, moving the country beyond pack assembly. Gotion High-Tech, through its NV Gotion joint venture with Nuovo Plus and GPSC, started battery-pack production in late 2023 with 2 GWh of Phase I capacity and a longer-term plan to cover up to 8 GWh of regional demand, supplying Neta and the broader ASEAN base. SVOLT, partnered with Banpu NEXT, reached its 10,000th locally produced pack by mid-2025, with output going into GWM’s ORA Good Cat, Haval H6 PHEV and Tank 300 HEV. BYD, separately, is integrating battery assembly directly inside its Rayong plant alongside vehicle production.

Battery cost typically runs at 30–40% of total BEV cost, so cell and pack localisation has an outsized effect on Thailand’s industrial depth. The country is now moving through pack assembly, into module and BMS work, and toward genuine cell manufacturing — in roughly that sequence.

Chassis and structural parts — the second wave

Chinese Tier-1s are also entering chassis and structural component manufacturing. Ningbo Tuopu Group, a major Chinese supplier of chassis systems, NVH parts, thermal management and interior modules, has signalled a Thailand investment of below USD 300 million, framed as supporting strategic customers outside China. The category that follows batteries usually includes front and rear axle modules, suspension links, subframes, brake and steering components, battery trays, underbody structures, lightweight aluminium parts and NVH/sealing systems. This is the segment where competition with Japanese, Thai and global Tier-1 incumbents will be most direct, because Toyota, Honda, Isuzu, Nissan and Mitsubishi platforms have anchored most of Thailand’s chassis supply for decades.

Power electronics, motors and BMS — next to scale

Battery management systems, traction motors, inverters, motor control units, DC-DC converters, on-board chargers and e-axles are all named or implied in Thailand’s BOI key-part list. Localisation here is still earlier than in battery packs, and most current BOI approvals in this category are for components rather than full e-powertrain systems. The acceleration window is 2026–2028, as Chinese OEMs move from initial assembly toward higher local content thresholds. Chinese suppliers have a structural advantage in this layer because their products are already integrated into BYD, GWM, Changan, GAC AION, SAIC-MG, Neta and Chery vehicle platforms.

Charging infrastructure and battery services

The BOI 2025 list includes multiple Chinese-affiliated charging-station and battery-swap projects, alongside a used-battery repair service centre operated by GAC Energy Technology. Cumulative BOI-approved investment across Thailand’s broader EV supply chain reached around THB 140 billion by late October 2025. As the EV parc grows, the centre of value will shift toward charging networks, diagnostics, battery repair, second-life ESS integration, warranty management and residual-value services — all of which Chinese OEMs prefer to bring with them rather than outsource.

Tires — older Chinese presence, now EV-relevant

Chinese tire makers were in Thailand long before the EV wave. Linglong’s Thai plant was the first overseas factory in its global footprint and the first Chinese tire plant in Thailand. Sentury and Prinx Chengshan also operate manufacturing capacity in the country. EV demand has made this presence more strategic, because EV tires require lower rolling resistance, higher load ratings and quieter cabin NVH — specifications that align with the original-equipment fitments Chinese OEMs already use on their platforms.

Interior, plastics and metalwork

The longest list of Chinese-affiliated BOI approvals sits in the most fragmented category. Vehicle parts, plastic interior and exterior components, alloy wheels, brake calipers, oil filters, drive shafts, suspension parts, seat covers, sealing strips and metalwork together account for the bulk of project numbers. Individually these are smaller investments, but together they represent the depth of Chinese supplier penetration into Thailand’s parts ecosystem — and the layer where Thai SMEs face the most direct competition.

What it means for Thailand’s legacy supplier base

The Japanese share of Thai vehicle production fell to around 78.5% in 2025, down from 86.6% in 2022. Chinese local production tripled year on year to roughly 106,000 units. Total Thai vehicle production in 2025 came in at about 1.46 million units, with Chinese OEMs and their affiliated suppliers accounting for the segment of clearest growth. The transition risk for Thailand’s legacy supplier base is therefore concentrated rather than evenly distributed.

Suppliers tied only to ICE pickups face the steepest adjustment

Pickup truck and ICE engine production is still the bulk of Thailand’s output, and that volume base is not collapsing. But the marginal new investment is going elsewhere. Suppliers concentrated in fuel systems, exhaust systems, transmission components and conventional engine parts are exposed to a long-term volume taper as electrified shares rise. Suppliers that have already diversified into thermal management, lightweight metals, electronics, plastics and sealing systems have more pathways into Chinese OEM platforms.

Thai SMEs can enter, mostly through partnership

BOI and provincial agencies are running structured business-matching programmes connecting Thai parts manufacturers to Chinese OEMs and their Tier-1 suppliers. The realistic near-term entry points for Thai SMEs are plastic mouldings, metal brackets, housings, harness work, aluminium parts, battery-pack casings, tooling, repair services and aftersales logistics — not battery cells, motor control units or BMS modules, where capability gaps are large and capital intensity is high. The medium-term path runs through joint ventures and technology-transfer arrangements with Chinese principals.

Risks worth watching

Four risks could change the speed or shape of this transition.

Demand-side weakness

Total Thai vehicle sales sat at roughly 633,000 units in 2025, broadly flat on 2024 and well below the 2022 level. Tight credit and elevated household debt continue to weigh on the broader market. Even with EV unit sales rising around 55% to roughly 200,000 units in 2025, an EV price war is putting pressure on margins. Suppliers may see volume growth without proportional margin growth.

Production driven by obligation, not demand

Some local EV production is being pulled forward by import-subsidy-linked production commitments rather than organic consumer demand. If retail demand softens further, suppliers risk underutilised capacity — especially in pack assembly and high-fixed-cost categories.

Policy revisions

Thailand has already adjusted EV policy once, allowing exported EVs to count toward production targets. Further revisions — in either direction — could reshape localisation timelines and content thresholds. Suppliers planning multi-year capacity build-outs need to assume some policy variance.

ASEAN competition

Indonesia, Malaysia and Vietnam are all competing for parts of the same Chinese EV supply chain. Indonesia has the nickel and battery-materials angle. Malaysia has electronics and semiconductors. Vietnam has VinFast and broader industrial momentum. Thailand’s structural advantage is its existing auto base — but only if policy stability holds.

The 2030 picture

Thailand has set a target of 30% electric-vehicle share of total vehicle production by 2030, against an installed-capacity assumption of around 2.5 million vehicles. That implies an EV production ambition close to 750,000 units a year. Even with realistic execution slippage, Thailand will be the largest EV manufacturing base in ASEAN, and the most likely regional export hub for Chinese-platformed electrified vehicles.

By 2030, the supplier mix supporting that production base is likely to look very different from today’s. Battery cells will be locally produced at meaningful volume. Battery packs and BMS will be standard local content. Traction motors, inverters and motor controllers will be at varying stages of localisation, with the most advanced Chinese OEMs running close to fully localised e-powertrains. Chassis and structural part suppliers will have built out alongside, and Thai SMEs will occupy the second-tier and Tier-3 layer in plastics, metalwork and packaging.

Bottom line

Chinese parts suppliers in Thailand are not a future development. They are the current direction of new investment. Battery localisation is already underway through Sunwoda, Gotion, SVOLT and BYD’s vertical integration. Chassis and structural component localisation is starting through Tuopu and a wider list of Chinese Tier-1s sitting inside the 2025 BOI approval set. Power electronics, motors and BMS will follow during 2026–2028, supported by BOI key-part rules that require local manufacturing within three years.

The structural shift is from a Japanese-led ICE supplier ecosystem to a hybrid ecosystem in which Japanese suppliers retain dominance in legacy ICE and pickup platforms while Chinese suppliers control the EV layer. Legacy Tier-1s with diversified portfolios will adapt. Suppliers concentrated only in ICE-specific components face a long taper. Thai SMEs face a transition risk and a participation opportunity at the same time — and which one materialises will depend less on policy ambition and more on capability building, JV formation and technology-transfer execution over the next thirty-six months.

─── END OF INSIGHT ───