Market Snapshot

Key Takeaways

Market Overview & Analysis

Report Summary

The India EV battery casing market covers the design, engineering, manufacturing, and supply of structural enclosures that house lithium-ion and other battery chemistries in electric vehicles. These casings — variously termed battery housings, battery enclosures, battery boxes, or battery trays — perform multiple critical functions: protecting cells from mechanical impact during collisions, sealing against moisture and environmental contaminants, integrating thermal management systems including liquid cooling channels, providing electromagnetic interference (EMI) shielding, and contributing to the vehicle's overall structural rigidity. The market spans raw material supply (aluminium alloys, high-strength steel, fibre-reinforced composites), component manufacturing (high-pressure die casting, stamping, extrusion, SMC moulding), and system integration (assembly of trays, covers, cooling plates, bus bars, and wiring harnesses).

India's battery casing landscape has entered a pivotal industrialisation phase. Until recently, the domestic market relied heavily on imported enclosures or simple fabricated metal boxes with limited engineering content. The shift toward dedicated EV platforms by OEMs like Mahindra (BE 6, XEV 9e), Tata Motors (Punch EV, Nexon EV), and global entrants has fundamentally elevated the complexity and strategic importance of battery housing as a structural, safety-critical component. The Hindalco–Mahindra partnership, Tata AutoComp's multi-material battery structure stack, Sundaram-Clayton's mega die-casting cluster, and Gestamp's fourth hot stamping line all signal a market moving from prototype-stage localisation into scaled, OEM-grade production. For broader context on India's rapidly evolving electric vehicle ecosystem, see the India Electric Three-Wheeler Market and India Electric Bus Market reports on Marqstats.

The India EV battery casing market sits at the intersection of two structural megatrends: India's accelerating vehicle electrification trajectory (EV market growing at 40.7% CAGR) and the global automotive lightweighting imperative that positions aluminium, composites, and hybrid-material housings as essential enablers of range extension and crash safety performance. As cell-to-pack (CTP) and cell-to-body (CTB) architectures gain adoption, the enclosure itself becomes an increasingly integrated part of the vehicle structure, amplifying its value share within the total battery pack cost.

Market Dynamics

Key Drivers

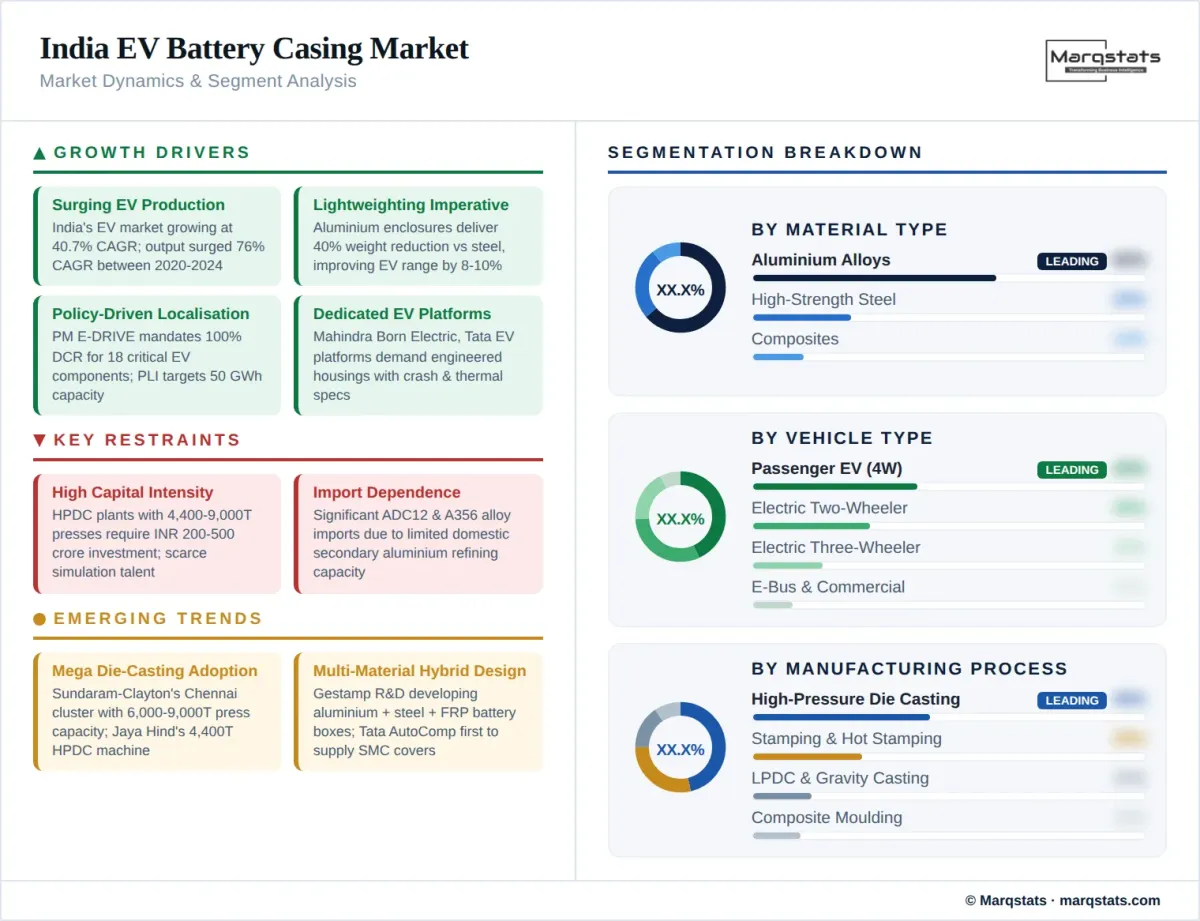

- Surging domestic EV production volumes — India's electric vehicle market was valued at USD 8.49 billion in 2024 and is projected to grow at a 40.7% CAGR through 2030. EV output surged at a 76% CAGR between 2020–2024, with EV components reaching 6% of total automotive part value. Each electric vehicle requires a purpose-built battery enclosure, creating a direct volume pull for casing manufacturers across all vehicle segments.

- Lightweighting imperative for range extension — Aluminium battery enclosures deliver up to 40% weight reduction compared to steel, translating to 8–10% improvement in driving range per vehicle. As OEMs develop dedicated EV platforms with 60–80 kWh battery packs for passenger vehicles, the weight and thermal performance of the enclosure becomes a critical engineering variable directly affecting vehicle competitiveness.

- Policy-driven localisation and domestic manufacturing mandates — The PM E-DRIVE scheme mandates 100% Domestic Content Requirement (DCR) for 18 critical EV components including battery packs. The PLI scheme for Advanced Chemistry Cells targets 50 GWh of domestic battery manufacturing capacity. The Phased Manufacturing Programme pushes progressive localisation of pack-level components including housings, trays, and thermal management systems, directly benefiting domestic enclosure manufacturers.

- OEM shift to dedicated EV platforms requiring engineered housings — As Mahindra, Tata Motors, and global OEMs move from converted ICE platforms to bespoke EV architectures (e.g., Mahindra's Born Electric platform with LFP battery systems co-developed with FEV Europe), the value and complexity of battery housings increases significantly. Structural integration, crash performance, sealing, and thermal management all become more demanding, favouring suppliers with advanced die-casting, composite, and multi-material capabilities.

- Crash safety regulations and GNCAP rating requirements — India's evolving Bharat NCAP and Global NCAP crash safety standards increase demand for high-performance battery enclosures that protect cells during side-impact and underbody collision scenarios. Hot-stamped steel and aluminium enclosures with integrated crash structures are becoming essential for achieving 4- and 5-star safety ratings in EVs.

Key Restraints

- High capital intensity of advanced die-casting infrastructure — Setting up high-pressure die-casting plants with 4,400T to 9,000T presses requires investments of INR 200–500 crore, creating significant entry barriers. Scarce simulation talent for die and tool design, expensive die-steel, and long development cycles for new enclosure programmes further constrain new entrants.

- Import dependence for high-grade aluminium alloys and composites — India imports a significant volume of ADC12 and A356 aluminium alloy ingots due to insufficient domestic secondary aluminium refining capacity. Specialty composites including carbon fibre and glass fibre reinforcements for battery covers also rely substantially on imports, exposing manufacturers to supply chain disruptions and currency fluctuation risks.

- Limited domestic EV four-wheeler production scale — While two-wheeler and three-wheeler EV volumes are high, the passenger car EV segment — which demands the most complex and high-value battery enclosures — is still scaling. This limits the addressable market for premium aluminium enclosure manufacturers like Hindalco, whose Chakan facility operates at 80,000 units annually against a domestic four-wheeler EV market that produced roughly 100,000 units in FY2025.

- Technology gap in cell-to-pack and cell-to-body integration — CTP and CTB architectures, which are being adopted globally by Tesla, BYD, and CATL, require enclosures that serve as structural load-bearing members of the vehicle chassis. Indian enclosure manufacturers are still developing capabilities in this area, creating a technology gap relative to Chinese and European suppliers.

Key Trends

- Mega die-casting and giga-stamping adoption — Sundaram-Clayton's new Thervoy Kandigai plant in Chennai, commissioned in January 2025 as India's largest integrated die-casting cluster, incorporates HPDC, LPDC, and gravity die casting with capacity for future 6,000T–9,000T presses. Jaya Hind Industries installed India's largest 4,400-tonne HPDC machine at its Urse, Pune plant in December 2024. These mega-casting investments enable single-piece structural battery housings that reduce part counts and assembly complexity.

- Multi-material hybrid battery housing designs — Gestamp's Indian R&D centre is developing multi-material battery boxes combining aluminium, high-strength steel, and fibre-reinforced plastic (FRP) — showcased for the first time at Auto Expo 2023. Tata AutoComp's composite division became the first in India to supply SMC (Sheet Moulding Compound) parts for EV battery packs, demonstrating that India's market is moving beyond pure-metal enclosures toward fire-safe composite covers and lids.

- Vertical integration by auto component majors — Uno Minda's INR 210 crore greenfield aluminium die-casting plant in Sambhaji Nagar (approved June 2025) supports backward integration for its planned 4W EV powertrain facility. Sandhar Technologies' subsidiary Sandhar Ascast acquired Sundaram-Clayton's Hosur HPDC/LPDC business for INR 163 crore, gaining access to higher-tonnage machines above 800T. These moves signal that battery housing is becoming a strategic component within broader EV powertrain integration strategies.

- Low-carbon and sustainable aluminium enclosures — Hindalco's Chakan plant uses low-carbon aluminium aligned with global sustainability benchmarks, reflecting the growing importance of Scope 3 emissions tracking by global OEMs. As export-oriented Indian EV suppliers target ASEAN and European markets under China-plus-one sourcing strategies, sustainable material credentials become a competitive differentiator for enclosure manufacturers.

Market Segmentation

Aluminium alloys dominate the India EV battery casing market with approximately 62% share in 2025, driven by their superior strength-to-weight ratio, excellent thermal conductivity for integrated cooling management, and corrosion resistance. Aluminium enclosures deliver up to 40% weight reduction over steel equivalents, directly improving EV driving range by 8–10%. Hindalco's Chakan facility (80,000 units/year, scalable to 160,000) and Sundaram-Clayton's mega die-casting cluster represent the most advanced domestic aluminium enclosure production capabilities. High-pressure die casting (HPDC) is the dominant manufacturing process, with semi-solid rheocasting gaining favour for premium battery housings requiring tighter tolerances. Al-Mg alloys providing electromagnetic shielding and crash energy absorption are emerging as the preferred formulations for EV-specific enclosures.

High-strength steel retains a significant market presence, particularly for cost-sensitive vehicle segments and applications requiring maximum crash performance. Steel enclosures are preferred where upfront tooling cost is a priority and where weight is a secondary consideration to impact resistance. Gestamp's hot stamping technology, deployed across four production lines in India (Pune and Chennai), enables the production of ultra-high-strength steel battery box components with tailored crash properties. Steel is especially relevant for commercial vehicles and lower-cost passenger EVs where the total cost of ownership equation favours steel over aluminium despite the weight penalty.

Composite battery casings — primarily glass fibre-reinforced plastic (GFRP) and carbon fibre-reinforced plastic (CFRP) — represent the fastest-growing material segment, projected to expand at a CAGR exceeding 21% during the forecast period. Tata AutoComp Composites Division became the first in India to supply SMC-technology battery covers for Tata Motors EV battery packs (November 2024), validating composites as a production-grade solution for fire-safe, lightweight battery lids. Globally, SGL Carbon's composite battery housing concepts demonstrate up to 50% weight reduction versus steel. Composites are particularly suited for battery pack covers and lids where fire retardancy, electrical insulation, and design flexibility are critical.

Passenger EVs represent the highest-value segment for battery enclosures due to the complexity and size of 40–80 kWh battery packs requiring engineered aluminium trays, composite covers, integrated cooling systems, and crash-optimised structures. The Hindalco–Mahindra partnership for the BE 6 and XEV 9e exemplifies the premium enclosure opportunity. As Tata Motors, Mahindra, Hyundai, and Maruti Suzuki expand their EV portfolios on dedicated platforms, the addressable market for advanced enclosures will scale significantly through 2030.

Electric two-wheelers represent the highest-volume segment by unit count, though individual enclosure value is lower due to smaller battery packs (1.5–4 kWh). Battery casings for 2W EVs are typically fabricated aluminium or plastic boxes with basic thermal management. The segment is driven by companies like Ola Electric, Ather Energy, TVS, and Bajaj, with growing demand for lightweight, compact enclosures compatible with both fixed and swappable battery architectures. For deeper analysis of the battery swapping ecosystem driving swappable-casing demand, see the India EV Battery Swapping Market report on Marqstats.

E-rickshaws and cargo three-wheelers constitute a large-volume segment with moderate enclosure complexity. Battery casings range from simple lead-acid battery boxes to more engineered lithium-ion enclosures with basic thermal management. Automotive Stampings and Assemblies (a Tata enterprise) has reported that its battery tray business is concentrated in e-cars and e-three-wheelers, confirming real volume pull from this segment beyond premium passenger EVs.

Electric buses and heavy commercial vehicles require the largest and most complex battery enclosures, often involving modular multi-pack configurations with advanced cooling systems. SUN Mobility's AIS-038-certified swappable battery platform for trucks and buses (50 kWh and 100 kWh variants at 660V) represents the emerging heavy-duty enclosure opportunity. The PM E-DRIVE scheme's allocation for electric bus procurement further supports demand growth in this segment.

HPDC is the dominant manufacturing process for aluminium battery enclosures, valued for its dimensional accuracy, production speed, and ability to produce thin-walled structural components at scale. India's HPDC capacity for EV components is expanding rapidly: Jaya Hind Industries installed a 4,400-tonne HPDC machine at Urse; Sundaram-Clayton's TKP facility can accommodate 6,000T–9,000T presses; and Samvardhana Motherson commissioned a 5,500-tonne press at its Aurangabad plant in 2025.

Stamping is widely used for steel and aluminium battery tray components, while hot stamping produces ultra-high-strength steel parts for crash-critical enclosure elements. Gestamp operates four hot stamping lines in India (three in Pune, one in Chennai) and has showcased extreme-size hot-stamped parts optimised for EV battery box simplification. Hot stamping is especially important for meeting GNCAP crash safety requirements in passenger EVs.

LPDC and gravity die casting are used for symmetric, lower-volume battery housing components requiring thicker walls and higher structural integrity. Sandhar Ascast's acquisition of Sundaram-Clayton's Hosur LPDC/HPDC business expanded access to LPDC technology for future battery-adjacent castings. These processes complement HPDC for components where porosity control and surface quality are paramount.

Sheet Moulding Compound (SMC) and Bulk Moulding Compound (BMC) processes are used for composite battery covers and lids. Tata AutoComp Composites deployed SMC technology for Tata Motors EV battery covers, producing parts that combine fire retardancy, electrical insulation, and design flexibility with lower tooling costs than metal stamping for complex cover geometries.

By Geography

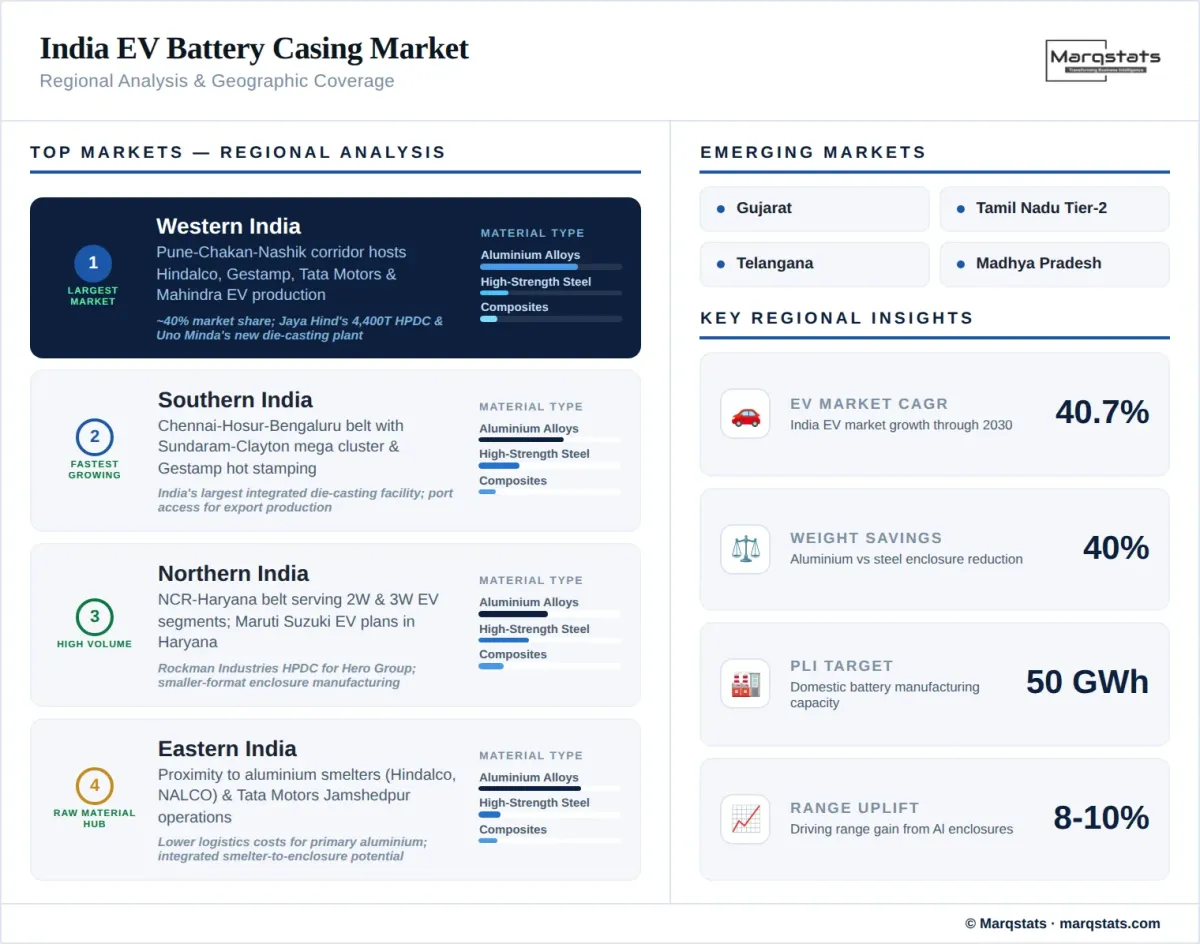

Western India (Pune–Chakan–Nashik Corridor)

Western India dominates the India EV battery casing market with approximately 40% share, anchored by the Pune–Chakan automotive cluster which hosts Hindalco's dedicated EV enclosure facility, Gestamp's hot stamping lines, Tata Motors' EV assembly operations, and Mahindra's electric SUV production. Jaya Hind Industries' Urse plant with India's largest 4,400T HPDC machine and Uno Minda's approved Sambhaji Nagar die-casting facility further strengthen the region's enclosure manufacturing capability. Proximity to major OEMs and a deep supplier ecosystem make Western India the primary production hub for passenger EV battery housings.

Southern India (Chennai–Hosur–Bengaluru)

Southern India is the fastest-growing region, driven by Sundaram-Clayton's mega die-casting facility in Thervoy Kandigai, Chennai — India's largest integrated die-casting cluster. The region hosts Gestamp's Chennai hot stamping line, Sandhar Ascast's acquired HPDC/LPDC operations at Hosur, and a growing concentration of EV component manufacturers serving Hyundai, Kia, TVS, and Ola Electric. Tamil Nadu's manufacturing incentives and port proximity for export-oriented production position Southern India as a critical growth corridor.

Northern India (Haryana–Rajasthan–UP)

Northern India serves the two-wheeler and three-wheeler EV segments with battery casing manufacturing concentrated in the NCR-Haryana belt. Maruti Suzuki's planned EV production in Haryana and Hero MotoCorp's electric two-wheeler operations drive demand for smaller-format enclosures. Rockman Industries (Hero Group) has scaled precision HPDC components for EV applications in this region.

Eastern India (Jamshedpur–Rourkela)

Eastern India's proximity to aluminium smelters (Hindalco, NALCO) provides raw material advantages for battery casing manufacturers. Tata Motors' Jamshedpur commercial vehicle operations and planned EV expansion create localised demand for heavy-vehicle battery enclosures. The region's lower logistics costs for primary aluminium make it attractive for integrated smelter-to-enclosure manufacturing models.

How Competition Is Evolving

The India EV battery casing market is in an early but fast-forming competitive phase, characterised by one clearly established commercial leader (Hindalco), a deep multi-material system integrator (Tata AutoComp), several casting-led capability builders positioning for future enclosure contracts (Sundaram-Clayton, Sandhar, Uno Minda, Jaya Hind), and global Tier-1 suppliers building India-specific EV housing platforms (Gestamp, Novelis, Nemak). Market concentration is still relatively low given the nascent stage of India's passenger EV production, but is expected to consolidate as OEM platform decisions lock in long-term enclosure supply relationships.

Hindalco Industries is the most advanced player in terms of a named OEM programme, visible production, and dedicated plant investment. Its INR 500 crore Chakan facility, co-developed with Mahindra, has delivered 10,000 enclosures with capacity to scale to 160,000 units annually, and plans to offer similar solutions to other Indian and global OEMs. Tata AutoComp occupies a strategically deeper position in battery-structure integration, spanning trays, composite covers, cooling tubes, plastic carriers, bus bars, and separators — making it the most comprehensive localised battery-pack structure supplier for mass-market e-cars and e-three-wheelers.

The casting-led challengers — Sundaram-Clayton, Sandhar Technologies, Uno Minda, Jaya Hind Industries, and Samvardhana Motherson — are building the industrial base required for future enclosure programmes through large-tonnage HPDC/LPDC capacity, EV-focused structural castings, and vertical integration. Their competitive positioning is currently capability-first and capacity-building, with named volume enclosure contracts expected to follow as India's passenger EV production scales beyond 200,000 units annually. Globally, Gestamp's Indian R&D centre with multi-material battery box prototypes and four hot stamping lines positions it as a significant contender for premium steel and hybrid-material enclosures.

Companies Covered

The report profiles 16++ companies with full strategy and financials analysis, including:

Recent Market Activity

Table of Contents

Coverage & Segmentation

This report provides a comprehensive analysis of the India EV battery casing market covering the historical period 2021–2025 and forecast period 2026–2030, with 2025 as the base year. The study encompasses market size and revenue projections, material segmentation (aluminium alloys, high-strength steel, composites), vehicle type analysis (passenger EV, two-wheeler, three-wheeler, bus and commercial vehicle), manufacturing process evaluation (HPDC, stamping, LPDC, composite moulding), and regional analysis across India's major automotive manufacturing corridors.

Primary research includes assessment of manufacturer capability announcements, OEM partnership disclosures, plant investment decisions, and technology development milestones across the battery enclosure supply chain. Secondary research draws from government policy documentation (PM E-DRIVE, PLI ACC, PMP), industry association data (SIAM, ACMA), company financial filings and press releases, die-casting industry publications, and trade media coverage. Market sizing employs bottom-up estimation based on EV production volumes, per-vehicle enclosure value by segment, and material mix analysis, validated against top-down industry benchmarks.