Market Snapshot

Key Takeaways

Market Overview & Analysis

Report Summary

The India electric truck market encompasses battery electric and fuel cell electric commercial vehicles designed for freight transportation across the full gross vehicle weight (GVW) spectrum from 3.5 tonnes to 55 tonnes, covering small commercial vehicles (SCVs below 3.5T), light commercial vehicles (LCVs 3.5–7.5T), intermediate commercial vehicles (ICVs 7.5–16T), and heavy-duty trucks (HDTs above 16T) including tippers, tractor-trailers, and rigid freight carriers. The market covers vehicle manufacturing, battery pack systems, powertrain integration, charging and swapping infrastructure, fleet financing models (vehicle-as-a-service, fleet leasing, battery-as-a-service), and the industrial application ecosystem spanning logistics, cement, ports, mining, steel, e-commerce, and FMCG supply chains.

India's electric truck landscape entered a pivotal commercialisation phase in 2025–26. The July 2025 launch of PM E-DRIVE's dedicated e-truck incentives — supporting N2 (3.5–12T) and N3 (12–55T) categories with subsidies capped at the lower of INR 5,000/kWh, 10% of ex-factory price, or a GVW-based ceiling reaching INR 9.6 lakh — provided the market's first structured policy stimulus. The scheme also mandated minimum warranty requirements (5 years / 5 lakh km for battery; 5 years / 2.5 lakh km for vehicle) and tied eligibility to phased localisation and commercial registration. However, a parliamentary committee review in March 2026 noted zero physical achievement for e-trucks under PM E-DRIVE as of January 2026, highlighting the gap between policy launch and on-ground deployment. For complementary analysis of the battery casing and enclosure technology underpinning these vehicles, see the India EV Battery Casing Market report on Marqstats.

The competitive landscape has broadened significantly. Tata Motors launched Trucks.ev in January 2026, calling it India's widest electric truck range spanning 7–55 tonnes. Montra Electric secured the first PM E-DRIVE-certified heavy-duty truck delivery to UltraTech Cement in January 2026. Ashok Leyland delivered its Boss Electric to BillionE and committed 180 electric trucks for the Chennai–Bengaluru intercity corridor. Eicher's Pro X EV completed the first commercially loaded Kashmir-to-Kanyakumari journey in February 2026. On the demand side, UltraTech Cement has emerged as India's clearest anchor customer with over 15 electric trucks operating across 17 manufacturing units and a target of 500 units, while JNPA's 50-truck fleet at Nhava Sheva with swappable batteries represents the strongest proof of heavy-duty operational deployment.

Market Dynamics

Key Drivers

- PM E-DRIVE's first dedicated e-truck subsidy scheme — The July 2025 launch provided India's first direct financial incentive for electric trucks, with support capped at INR 9.6 lakh for N3 category vehicles. The scheme targets deployment of 5,600 e-trucks and allocated approximately INR 500 crore for the segment. Mandatory scrapping certificates for old trucks, minimum warranty requirements, and phased localisation mandates create a structured framework that improves OEM and fleet operator confidence. Delhi alone allocated INR 100 crore for 1,100 e-truck deployments.

- TCO advantage in high-utilisation industrial routes — Electric trucks deliver lower per-kilometre operating costs through reduced fuel and maintenance expenses compared to diesel equivalents. The ROI for heavy-duty electric trucks deployed in correct applications is estimated at 3–4 years. Electric tippers' after-sales costs are approximately 60–70% lower than diesel equivalents, making them compelling for cement, port, and mining fleet operators with predictable, high-utilisation routes. Major fleet owners are planning to electrify up to 20% of their total fleet by FY2030.

- Fixed-route industrial adoption from cement, ports, and mining sectors — The heavy-duty electric truck market is projected to grow at 35.5% CAGR in cement, 31.5% in ports, and 27% in mining through FY2030. These industries operate on controlled, repetitive routes with predictable daily mileage, making them ideal for battery-electric operations. UltraTech Cement is targeting 500 electric trucks, SAIL has proposed 150 electric trucks in its initial procurement phase, and GreenLine Mobility partnered with Hindustan Zinc for 100 electric trucks between mines and smelters.

- OEM product portfolio expansion across the full GVW range — India's electric truck product landscape has rapidly expanded from a handful of LCV/SCV models to full-spectrum coverage. Tata Motors' Trucks.ev spans 7–55 tonnes, Ashok Leyland offers the Boss Electric 14T and AVTR 55T tractor, Eicher's Pro X covers 2–3.5 tonnes, Montra's Rhino range includes 28T tippers and 55T heavy trucks, and Mahindra's Zeo achieved 1,245 units sold in May–July 2025 with 188% year-on-year growth. Price range spans INR 13.75 lakh (SCV) to INR 1.55 crore (HD tipper).

- PLI schemes and domestic manufacturing acceleration — The PLI scheme for auto components (INR 25,938 crore) and PLI for Advanced Chemistry Cells incentivise domestic manufacturing of EV trucks and their battery packs. Ashok Leyland inaugurated a new EV-focused commercial vehicle plant in Lucknow in January 2026. The March 2026 PM E-DRIVE amendment tightened localisation requirements, making domestic manufacturing of traction motors mandatory from September 2026 for specified components.

Key Restraints

- Inadequate charging infrastructure for commercial trucking — Only about 5% of India's EV chargers are capable of meeting zero-emission truck power requirements. Heavy-duty trucks require high-power DC fast charging (150–350 kW) or battery swapping stations, both of which are scarce along freight corridors. India's first commercial heavy-duty e-truck battery swapping station opened only in October 2025 at Sonipat, Haryana, highlighting the infrastructure gap.

- High upfront vehicle cost versus diesel equivalents — Electric truck prices are approximately twice that of equivalent diesel trucks, with batteries accounting for 40–50% of total vehicle cost. While TCO advantages exist over 3–4 years in high-utilisation routes, the higher upfront capital requirement creates financing barriers, particularly for individual truck owner-operators who control approximately 64% of India's truck fleet.

- Zero physical achievement under PM E-DRIVE as of January 2026 — Despite the policy launch in July 2025, a parliamentary committee review reported nil physical achievement for e-trucks under PM E-DRIVE as of January 2026. This gap between policy announcement and on-ground deployment reflects the time needed for OEM certification, fleet operator decision-making, and subsidy disbursement mechanics to align.

- Limited long-haul viability for heavy-duty battery electric trucks — Current battery technology constrains heavy-duty electric truck range to 150–300 km per charge depending on payload, insufficient for India's typical 400–800 km intercity freight routes. While battery swapping addresses this for fixed routes, open-market long-haul trucking remains impractical for BEV technology in the near term without corridor-level charging or swapping infrastructure.

Key Trends

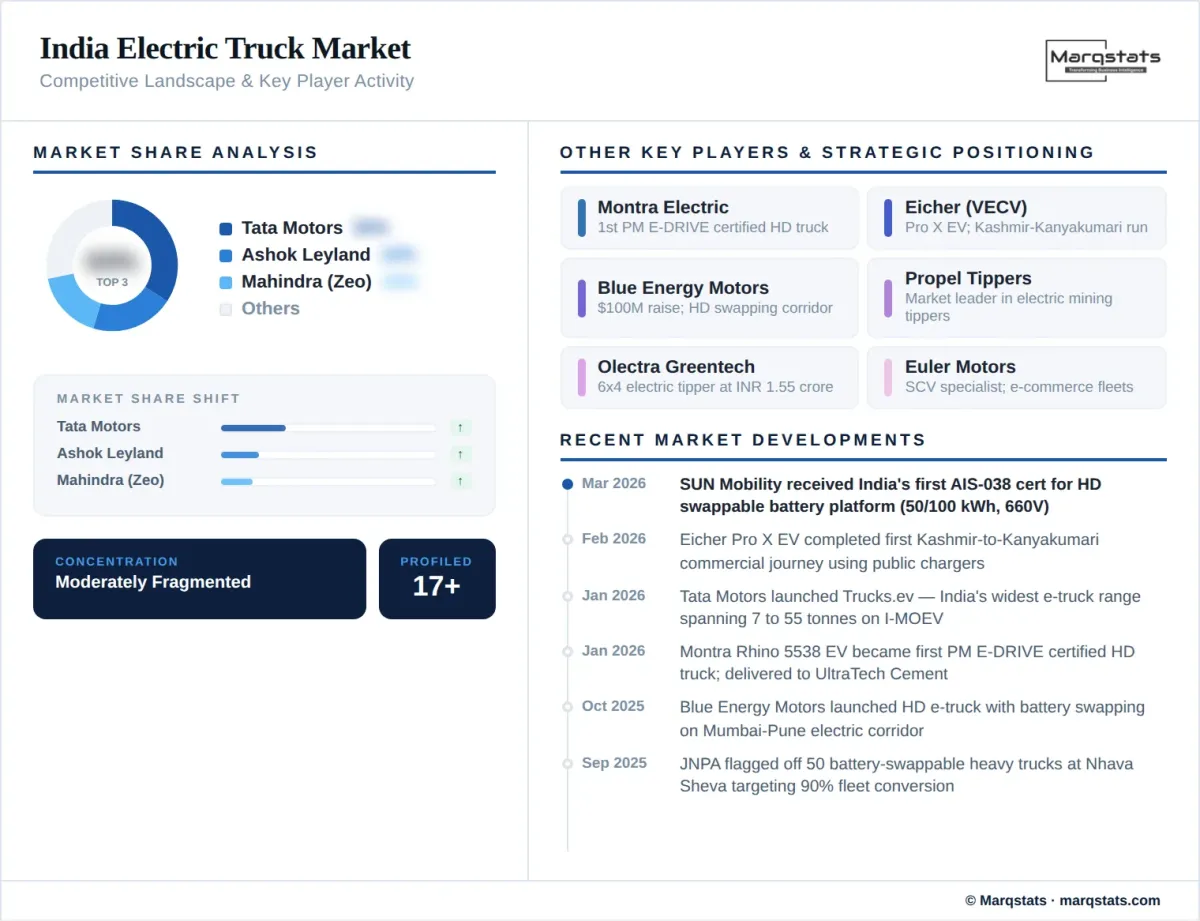

- Battery swapping corridors for heavy-duty freight — Heavy-duty electric trucking in India is increasingly being built around fixed-route, high-uptime, swapping-compatible use cases. Blue Energy Motors launched a heavy-duty e-truck with battery swapping linked to a Mumbai–Pune electric corridor in October 2025. JNPA's Nhava Sheva fleet uses swappable batteries with 7-minute swap cycles. SUN Mobility's March 2026 AIS-038 certification for a 50/100 kWh high-voltage swappable platform (660V) validates heavy-duty swapping as a compliant commercial pathway.

- Anchor customer model driving adoption ahead of open market — Unlike passenger EVs, electric truck adoption is being pulled by named industrial anchor customers. UltraTech Cement (targeting 500 trucks), SAIL (proposed 150 trucks), JNPA (targeting 90% fleet conversion), GreenLine Mobility + Hindustan Zinc (100 trucks), and BillionE (250+ fleet contracts) demonstrate that demand-side aggregation and route-specific deployment are more important than open-market retail sales.

- Fleet financing and vehicle-as-a-service models emerging — In Indian freight, financing and operator aggregation are almost as important as OEM launches. BillionE secured 250+ fleet contracts for commercial electric trucks around PM E-DRIVE's launch. Vehicle-as-a-Service (VaaS), fleet leasing, and Battery-as-a-Service (BaaS) models are emerging to address the high upfront cost barrier, enabling fleet operators to pay per kilometre or per tonne rather than purchasing outright.

- Electric tipper trucks gaining traction in mining and cement — Propel Tippers has emerged as market leader in electric tippers aligned with mining requirements. Olectra launched a 6x4 electric tipper at INR 1.55 crore. The GVW 45+ tonne segment is most attractive for electric tippers because ROI is achievable in 3–5 years. Electric tippers are projected to capture 30–40% of the mining tipper market by 2030, driven by 60–70% lower after-sales costs.

Market Segmentation

The SCV segment is the most commercialised electric truck category in India, led by Tata Ace EV, Mahindra Zeo, Euler Storm, and OSM Rage Plus. Mahindra's Zeo achieved breakout performance with 1,245 units sold in May–July 2025 and 188% year-on-year growth, offering 160 km range with a 7-year warranty. The segment is primarily driven by last-mile e-commerce delivery, FMCG distribution, and urban parcel logistics where depot charging is workable and daily distance requirements fit current battery capabilities.

The LCV segment is scaling through urban and near-city cargo applications. Eicher's Pro X EV (2–3.5T segment) has been deployed with Pickkup for 100 units across Delhi-NCR and Bengaluru serving retail, e-commerce, FMCG, and perishable logistics. Switch Mobility (Ashok Leyland's EV arm) achieved 266% year-on-year growth in e-LCV sales in 2025. This segment benefits from proven urban logistics economics and growing GNCAP safety requirements.

The ICV segment represents a bridging category between urban delivery and heavy freight. Ashok Leyland's Boss 1218 HB EV and Boss 14T — India's first electric ICV — target this segment for hub-to-hub distribution and industrial material movement. The ICV is increasingly attractive for intra-city construction material transport and industrial supply chains where route predictability supports electric viability.

The heavy-duty segment is the market's breakthrough growth story, projected to reach USD 1.23 billion by FY2030 at a 55% CAGR. The segment is split between tippers (mining, cement, port operations) and tractor-trailers (container movement, intercity logistics). Tata's Prima E.28K, Montra's Rhino 5538 EV (first PM E-DRIVE-certified HDT), Ashok Leyland's AVTR 55T, and BYD's electric tractor-trailer represent the competitive frontier. JNPA's 50-truck swappable-battery fleet at Nhava Sheva is the strongest operational proof point for HD electric trucking in India.

Last-mile delivery is the largest application by unit volume, driven by fleet electrification commitments from Amazon, Flipkart, Swiggy, and Zomato. The segment primarily uses SCV and LCV electric trucks (below 7.5T) with depot charging. Tata Ace EV, Mahindra Zeo, and Euler Storm are the primary suppliers. Eicher's partnership with Pickkup for 100 Pro X EVs across Delhi-NCR and Bengaluru exemplifies the scaling pattern in this application.

Cement is the highest-growth application for heavy-duty electric trucks at a projected 35.5% CAGR through FY2030. UltraTech Cement is the anchor customer, with over 15 electric trucks across 17 manufacturing units and a target of 500 trucks under its eFAST initiative. UltraTech introduced five electric trucks for clinker movement between Dhar and Dhule units as early as January 2024, and inducted Montra's PM E-DRIVE-certified Rhino 5538 EV in January 2026. Sagar Cement, Adani, and JSW have also expressed interest in fleet electrification.

Port logistics represents a 31.5% CAGR application, with JNPA's deployment of 50 battery-swappable heavy electric trucks at Nhava Sheva (September 2025) as the defining proof point. JNPA targets conversion of 90% of its approximately 600 internal heavy trucks by December 2026. Controlled port routes, predictable duty cycles, and high utilisation rates make ports ideal for electric heavy trucking. BYD is reportedly in discussions for over 400 electric tractor-trailers for port and cement applications.

Mining is a 27% CAGR application driven by electric tippers operating on fixed haul routes between mines, processing facilities, and loading points. Propel Tippers is the market leader in electric tippers aligned with mining requirements. GreenLine Mobility partnered with Hindustan Zinc for 100 electric trucks between mines and smelters. SAIL has proposed procurement of 150 electric trucks in its initial phase. The GVW 45+ tonne electric tipper is the most attractive mining segment with 3–5 year ROI.

Intercity logistics is emerging but faces infrastructure constraints. Ashok Leyland committed 180 electric trucks to BillionE for the Chennai–Bengaluru corridor — India's largest intercity e-truck deployment. Blue Energy Motors launched a heavy-duty e-truck with battery swapping on the Mumbai–Pune corridor. Eicher's Pro X EV completed the Kashmir-to-Kanyakumari journey in February 2026, validating small-truck long-distance feasibility using public chargers.

By Geography

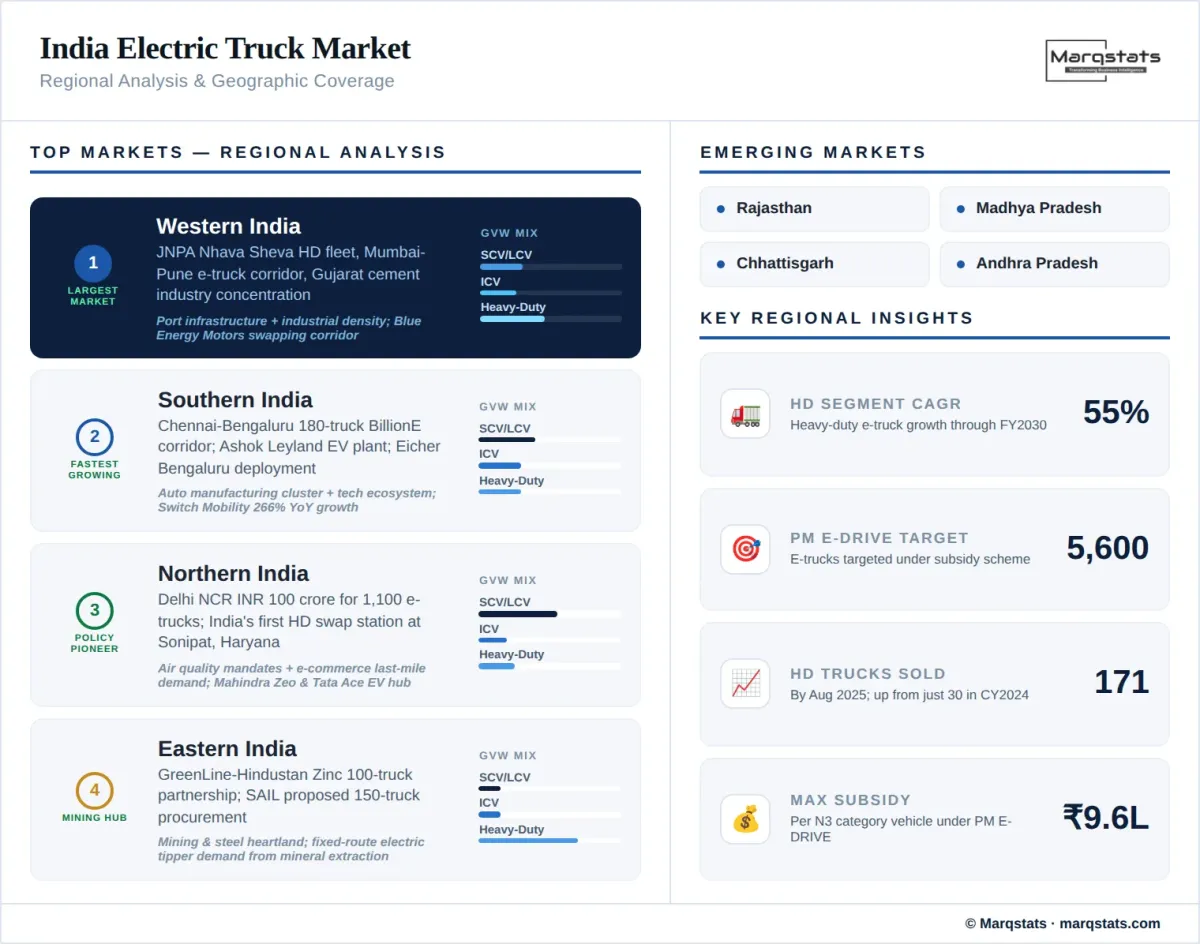

Western India (Maharashtra–Gujarat)

Western India leads the India electric truck market, anchored by JNPA's Nhava Sheva heavy-duty fleet deployment, the Mumbai–Pune electric truck corridor initiative, and Gujarat's cement industry concentration with UltraTech's e-truck operations between Dhar and Dhule. Maharashtra hosts Blue Energy Motors' swapping-focused corridor deployment and key OEM assembly operations. The region's port infrastructure, industrial manufacturing density, and highway connectivity make it the primary adoption corridor for heavy-duty electric trucking.

Southern India (Tamil Nadu–Karnataka–Andhra Pradesh)

Southern India is the fastest-growing region, driven by the Chennai–Bengaluru intercity corridor (Ashok Leyland's 180-truck BillionE deployment), Ashok Leyland's new EV-focused commercial vehicle plant in Lucknow and Switch Mobility's operations, and Eicher's Pickkup deployment of 100 Pro X EVs in Bengaluru. BYD's electric tractor-trailer discussions reference Vizag port operations. Tamil Nadu's auto manufacturing cluster and Karnataka's technology ecosystem create a strong supply-demand nexus for electric trucking.

Northern India (Delhi NCR–Haryana–UP)

Delhi NCR is a high-priority deployment zone with INR 100 crore allocated for 1,100 e-trucks. India's first commercial heavy-duty e-truck battery swapping station opened in Sonipat, Haryana in October 2025. The region's severe air quality challenges, stringent vehicular emission regulations, and dense last-mile delivery networks driven by e-commerce create strong pull for both SCV electric trucks (Tata Ace EV, Mahindra Zeo) and heavy-duty electrification in industrial corridors.

Eastern India (Jharkhand–Odisha–West Bengal)

Eastern India represents an emerging market driven by mining-sector electrification demand. GreenLine Mobility's partnership with Hindustan Zinc for 100 electric trucks between mines and smelters, and SAIL's proposed 150-truck procurement signal demand activation in the mining and steel heartland. The region's concentration of mineral extraction and heavy industrial operations creates specific demand for electric tippers and haul trucks on fixed routes.

How Competition Is Evolving

The India electric truck market features a mix of established commercial vehicle OEMs extending into electric, pure-play EV truck startups, and emerging Chinese entrants. Tata Motors holds the broadest disclosed portfolio with its Trucks.ev range spanning 7–55 tonnes on the I-MOEV architecture, covering mini trucks, pickups, intermediate, and heavy trucks for e-commerce, construction, and port applications. Ashok Leyland was an early mover with the Boss Electric 14T and AVTR 55T platforms, and committed India's largest intercity e-truck deployment of 180 trucks to BillionE on the Chennai–Bengaluru corridor. Eicher (VECV joint venture with Volvo) is strongest in urban and near-city cargo with the Pro 2055 EV and Pro X EV.

Montra Electric has established itself as the sharpest heavy-duty pure-play specialist, securing the first PM E-DRIVE-certified heavy-duty truck delivery to UltraTech Cement and becoming the first OEM to partner with the government-backed NHEV initiative targeting 1,000+ electric trucks. In the SCV segment, Mahindra's Zeo achieved breakout sales of 1,245 units in May–July 2025 with 188% year-on-year growth. Propel Tippers leads in electric mining tippers, while Olectra has entered with a 6x4 electric tipper at INR 1.55 crore. Blue Energy Motors, pivoting from LNG with a $100 million fundraise, launched a heavy-duty e-truck with battery swapping linked to the Mumbai–Pune corridor. For analysis of the battery swapping infrastructure supporting heavy-duty e-truck operations, see the India EV Battery Swapping Market report on Marqstats.

Beyond OEMs, ecosystem players are shaping market structure. UltraTech Cement acts as India's strongest anchor customer. JNPA serves as the primary port logistics proving ground. SUN Mobility provides certified heavy-duty swapping technology with the AIS-038-certified 50/100 kWh platform. BillionE solves fleet aggregation and financing, having secured 250+ fleet contracts. In Indian freight, these demand-side and infrastructure players matter as much as vehicle launches because adoption depends on route economics, energy access, uptime, and contract structures.

Companies Covered

The report profiles 17+ companies with full strategy and financials analysis, including:

Recent Market Activity

Table of Contents

Coverage & Segmentation

This report provides a comprehensive analysis of the India electric truck market covering the historical period 2021–2025 and forecast period 2026–2030, with 2025 as the base year. The study examines market size and revenue projections, GVW-based segmentation (SCV, LCV, ICV, HDT), application analysis (last-mile delivery, cement, ports, mining, intercity logistics), powertrain evaluation, regional deployment patterns, competitive landscape across OEMs and ecosystem players, and policy impact assessment including PM E-DRIVE e-truck incentives, PLI schemes, and localisation mandates.

Primary research includes assessment of OEM product launches, fleet deployment milestones, industrial anchor customer commitments, government subsidy mechanics, and infrastructure development across charging and swapping networks. Secondary research draws from parliamentary committee reports, PM E-DRIVE operational guidelines and portal amendments, industry sales data, OEM press releases and annual filings, port authority disclosures, and trade media coverage. Market sizing employs bottom-up estimation based on vehicle segment sales volumes, per-unit revenue by GVW class, and application-specific deployment forecasts, validated against top-down industry benchmarks.