Market Snapshot

Key Takeaways

Market Overview & Analysis

Report Summary

The India electric three-wheeler market report provides a comprehensive analysis of the manufacturing, retail, deployment, and operation of electrically propelled three-wheelers across passenger transit, cargo logistics, and last-mile delivery applications. The scope covers e-rickshaws (top speed <25 km/h), L5-category electric auto rickshaws (licensed for higher speeds, route permits, and insurance), electric cargo/goods carriers, and e-carts. The market is segmented across seven dimensions: by vehicle type (e-rickshaw, L5 passenger e-auto, L5 cargo, e-cart), by battery type (lead-acid, lithium-ion LFP, lithium-ion NMC), by motor type (BLDC hub motor, mid-drive motor, differential motor), by power output, by voltage capacity, by driving range, and by region (North, South, East, West India). The study covers 2021–2030, with 2025 as the base year.

India is the world’s largest market for electric three-wheelers. In FY2024–25, the segment recorded approximately 699,073 unit sales and accounted for 57% of all three-wheeler registrations across all powertrains. EV penetration in the L5 passenger three-wheeler sub-category reached 22.8% in FY2025 — significant given that L5 is a more regulated and higher-value segment than e-rickshaws. The overall electric three-wheeler share of 60.91% in CY2025 makes this category’s EV penetration the highest of any vehicle segment in India. The India electric three-wheeler market analysis reveals a sector at a critical inflection point: the transition from an unorganised, lead-acid-powered e-rickshaw assembler base toward an organised, lithium-ion-powered, warranty-backed product ecosystem led by India’s largest automotive groups. This structural shift is creating a dual market — the legacy e-rickshaw segment with low ASPs (INR 80,000–150,000) and the premium L5 segment with higher ASPs (INR 2.5–5 lakh) — with profoundly different growth dynamics.

The latest monthly data confirms sustained momentum: in January 2026, EV share in total three-wheeler retail was 59.61% (e-rickshaw passenger: 44,456 units; e-rickshaw with cart: 7,656 units). In February 2026, EV share was 56.70% (e-rickshaw passenger: 34,848 units; e-rickshaw with cart: 7,268 units). For FY26 YTD (April 2025–February 2026), total India three-wheeler retail stood at 12,53,658 units, up 11.78% YoY.

Market Dynamics

Key Drivers

- Unmatched EV penetration and structural cost advantage: Electric three-wheelers offer substantially lower per-kilometre operating costs compared to CNG and diesel alternatives — electricity costs INR 0.50–0.80/km versus INR 2–3/km for CNG, delivering savings of INR 40,000–60,000 annually for a typical owner-driver operating 80–100 km daily. Maintenance costs are 60–70% lower due to fewer moving parts. This TCO advantage is the primary adoption driver, particularly in tier-2 and tier-3 cities where operators work on thin margins.

- PM E-DRIVE scheme incentivising 3.2 lakh electric three-wheelers: The PM E-DRIVE scheme (launched October 2024, extended to March 2028) provides structured subsidies: e-rickshaws receive INR 25,000 per unit in FY2025, reduced to INR 12,500 in FY2026; L5 cargo three-wheelers qualify for INR 50,000 (FY25) and INR 25,000 (FY26). As of 27 January 2026, 2.93 lakh e-three-wheelers had been sold under PM E-DRIVE. However, a Parliamentary committee note (March 2026) reveals the outcome is heavily skewed toward L5 vehicles: 2,21,600 e-3W L5 units versus only 3,602 e-rickshaw/e-cart units against a revised target of 39,034. The subsidy tapering signals the government’s view that the market is approaching commercial self-sustainability.

- Entry of organised legacy OEMs transforming product quality: Mahindra Last Mile Mobility (India’s number-one electric commercial vehicle manufacturer for the fourth consecutive year in FY2025, surpassing 300,000 cumulative EV deliveries by November 2025), Bajaj Auto (launched the GoGo brand in February 2025 with three passenger variants offering 251 km certified range and a 5-year battery warranty from INR 3.27 lakh), TVS Motor (entered January 2025 with King EV MAX at 179 km certified range, INR 2.95 lakh), and Piaggio (Ape E-City Ultra launched July 2025 with 236 km certified range / approximately 205 km real-world range using LFP chemistry) are collectively raising product standards, build quality, and consumer confidence.

- Rising fuel costs accelerating substitution: In April 2025, the Indian government hiked excise duty on petrol and diesel by INR 2 per litre each. This directly impacts auto-rickshaw operators’ economics, making electric alternatives more attractive. CNG price volatility in Delhi-NCR and Mumbai corridors further strengthens the economic case for electrification.

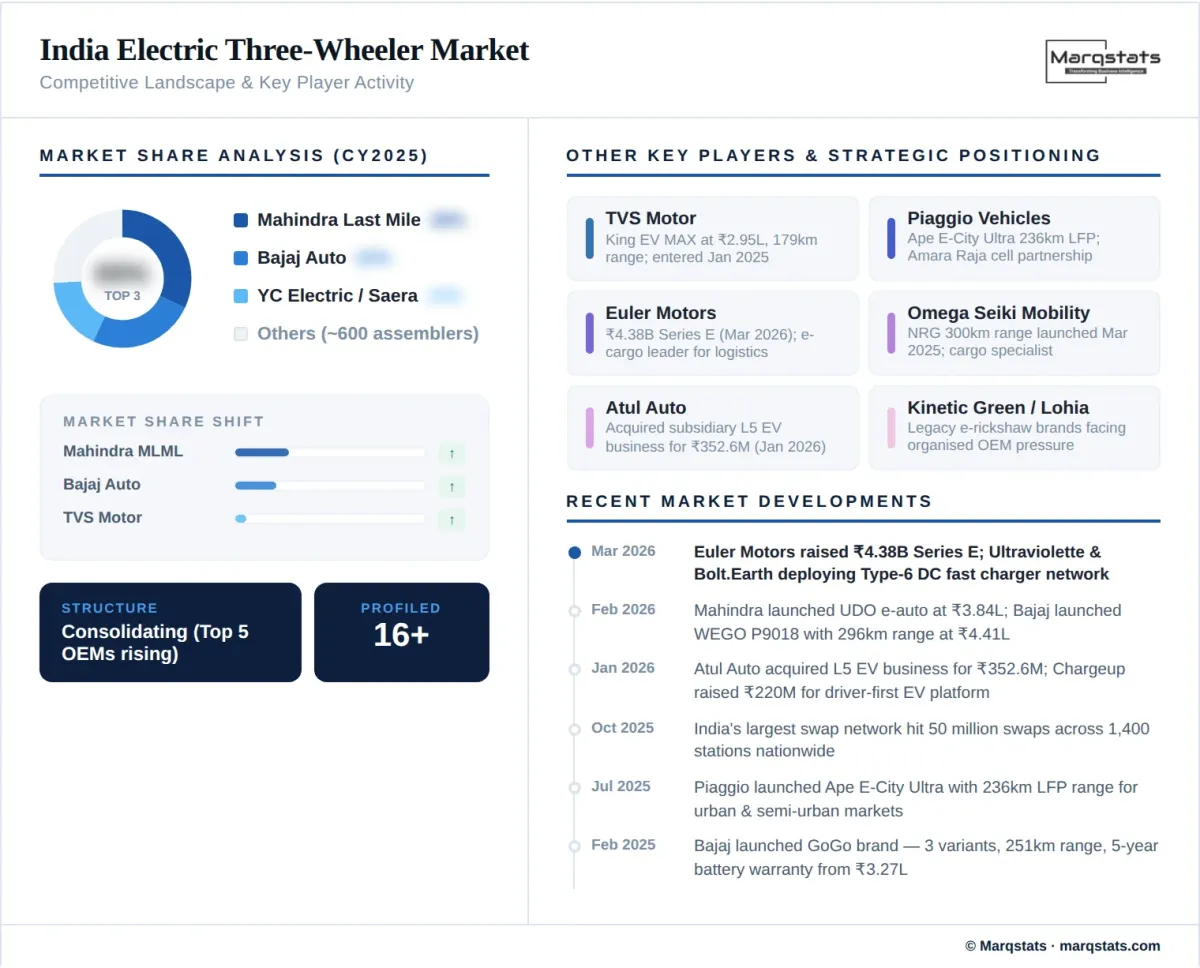

- Last-mile e-commerce logistics demand expansion: E-commerce delivery platforms are rapidly adopting electric cargo three-wheelers for hyperlocal and last-mile logistics. Borzo launched an e-three-wheeler fleet in Mumbai in January 2025. Amazon, Flipkart, and BigBasket are expanding electric cargo fleets. Euler Motors raised INR 4.38 billion in Series E funding (March 2026) specifically to scale electric three-wheeler and four-wheeler manufacturing and expand its India presence.

Key Restraints

- Severe charging infrastructure deficit: India has approximately 11,000 public EV chargers nationally (across all vehicle types), with virtually no dedicated three-wheeler charging network at scale. Most e-rickshaw charging relies on informal roadside connections using domestic power outlets, raising safety and grid-load concerns. A recent Parliamentary reply confirmed that no charging stations had been installed under PM E-DRIVE as of early 2026. Formal depot-level charging for commercial three-wheeler fleets remains underdeveloped outside major metros, creating a structural bottleneck for fleet-scale electrification.

- Lead-acid to lithium-ion transition cost barrier: Lead-acid batteries still command approximately 64.68% of the installed base due to their low upfront cost (INR 15,000–25,000 per pack versus INR 50,000–80,000 for lithium-ion). While lithium-ion offers superior energy density, cycle life (2,000–3,000 cycles vs 300–500), and range, the 2–3x cost premium remains a barrier for price-sensitive e-rickshaw operators in North and East India.

- Unregistered e-rickshaw fleet and safety concerns: An estimated 4.75 lakh unregistered e-rickshaws operate without certification, registration, or insurance. This shadow fleet creates safety risks, depresses pricing for organised OEMs, and complicates market sizing. Government efforts to bring unregistered vehicles into the formal fold through amnesty registrations and enforcement drives are progressing unevenly across states.

- PM E-DRIVE subsidy underperformance in e-rickshaw/e-cart segment: Despite 2.93 lakh e-three-wheelers sold under PM E-DRIVE overall, the e-rickshaw and e-cart sub-category registered only 3,602 units against a revised target of 39,034 as of 31 January 2026. This suggests the subsidy structure (INR 12,500 per unit in FY2026) may be insufficient for this price-sensitive segment, and that the scheme’s distribution and awareness mechanisms for unorganised-sector operators need strengthening. Owner-driver financing constraints and limited access to formal credit channels further slow adoption among the target demographic.

Key Trends

- Organised versus unorganised market consolidation: The Vahan portal lists nearly 600 registered three-wheeler manufacturers, the vast majority being small-scale e-rickshaw assemblers in North and East India. However, Bajaj Auto recorded 330% YoY growth in April 2025 (5,509 units), separated from Mahindra by just 131 units in monthly sales. TVS, Piaggio, Atul Auto, and the Murugappa Group’s TI Clean Mobility are also scaling rapidly. This organised-versus-unorganised dynamic is a defining structural feature and a consolidation opportunity.

- Battery swapping as infrastructure game-changer: India’s largest three-wheeler battery swap network completed 50 million swaps across 1,400 stations as of October 2024. Honda Power Pack Energy India is targeting 500 e:Swap stations across Bengaluru, Delhi, and Mumbai by March 2026. The Battery-as-a-Service (BaaS) model is gaining traction: Mahindra Last Mile Mobility partnered with Vidyut (December 2024) to offer BaaS financing for the Zor Grand and Treo Plus, separating battery ownership from vehicle purchase to reduce upfront cost. Ultraviolette partnered with Bolt.Earth (March 2026) to roll out a nationwide network of Type-6 DC fast chargers for light EVs including electric three-wheelers.

- Fleet-as-a-Service (FaaS) and fintech innovation: Managed mobility models that separate vehicle ownership from fleet operation are emerging, particularly for e-commerce logistics. Chargeup raised INR 220 million (January 2026) to scale its driver-first EV tech platform for three-wheelers. Fintech lending platforms are expanding credit access for owner-driver operators who typically lack formal credit histories.

- Lithium-ion LFP technology transition accelerating: LFP chemistry is gaining share due to superior thermal stability, longer cycle life, and declining costs. Piaggio partnered with Amara Raja for LFP cells (August 2024). Bajaj standardised GoGo on LFP across all variants. Luminous Power Technologies inaugurated a lithium-ion battery assembly line at Baddi, Himachal Pradesh, with 500 MWh capacity (January 2026) specifically supporting electric three-wheelers. Tsuyo Manufacturing launched Gen 3.0 IPM motor and controller architecture for e-three-wheelers (February 2026).

- Export market emergence: Bajaj Auto is explicitly targeting electric three-wheeler export markets including Nepal, Bangladesh, and Africa by 2026. India’s cost-competitive manufacturing base, established supply chains, and high-volume production experience position the country as a natural export hub for affordable electric three-wheelers across South Asia and sub-Saharan Africa.

Market Segmentation

E-rickshaws (passenger) dominate the India electric three-wheeler market with 4,76,936 units retailed in CY2025, representing the single largest product category. These are low-speed vehicles (top speed <25 km/h) used primarily for first-mile and last-mile connectivity to metro stations, bus stops, and railway stations in North and East India. E-rickshaws operate under a simplified regulatory framework (no commercial driving licence required in most states) and are priced between INR 80,000–1,50,000, making them affordable for owner-drivers. However, the segment faces challenges from unregistered operators, lead-acid battery reliance, and safety concerns.

E-rickshaw with cart (goods) retailed 83,403 units in CY2025, serving last-mile cargo movement for vegetables, parcels, and small goods in urban and semi-urban areas. This segment is growing faster than passenger e-rickshaws as e-commerce platforms and hyperlocal delivery services increasingly adopt electric cargo three-wheelers. The goods carrier segment is projected to register the fastest CAGR, driven by rising urbanisation, government incentives (INR 50,000 subsidy for L5 cargo under PM E-DRIVE in FY2025), and operational cost efficiency.

L5-category electric auto rickshaws are transforming the market’s premium segment. Unlike e-rickshaws, L5 vehicles operate at higher speeds (40–70 km/h), require commercial driving licences, carry route permits, and use lithium-ion batteries. EV penetration in the L5 passenger sub-category reached 22.8% in FY2025, representing significant traction in this more regulated segment. Key products include Bajaj GoGo (three variants, 251 km certified range, INR 3.27 lakh onwards), Bajaj WEGO P9018 (296 km certified range, 17.7 kWh, INR 4.41 lakh, launched February 2026), Mahindra Treo (139 km ARAI-certified / approximately 110 km real-world, 7.4 kWh) and Treo Plus (167 km ARAI-certified / approximately 150 km real-world, 10.24 kWh), Mahindra UDO (introductory price INR 3,58,999, launched February 2026), TVS King EV MAX (179 km certified range, INR 2.95 lakh), and Piaggio Ape E-City Ultra (236 km certified / approximately 205 km real-world, LFP chemistry).

L5 electric cargo three-wheelers serve the growing e-commerce last-mile delivery segment. Key players include Euler Motors (raised INR 4.38 billion Series E in March 2026), Mahindra Zor Grand, Piaggio Ape E-Xtra, Omega Seiki NRG (300 km certified range, launched March 2025), and Montra Electric Super Cargo. This segment benefits from the strongest subsidy support (INR 50,000 under PM E-DRIVE in FY2025) and addresses the growing demand from e-commerce logistics, quick-commerce platforms, and municipal solid waste management.

Lead-acid batteries account for approximately 64.68% of the installed base, predominantly in the e-rickshaw segment where low upfront cost (INR 15,000–25,000 per battery pack) takes priority over performance. Lead-acid packs offer 300–500 cycles, 40–70 km range, and require replacement every 8–12 months under heavy commercial use. The segment is declining as lithium-ion prices fall and organised OEMs standardise on LFP chemistry.

Lithium-ion batteries — particularly LFP chemistry — are projected to grow at over 21% CAGR through 2030 as pack prices continue to decline. Global battery cell costs dropped from approximately USD 110/kWh in mid-2023 to approximately USD 56/kWh by mid-2024. In India, LFP packs for three-wheelers cost INR 50,000–80,000 but offer 2,000–3,000 cycles, 100–300 km range, and 3–5 year lifespans. All organised L5 OEMs now standardise on lithium-ion. The Piaggio–Amara Raja LFP collaboration, Bajaj’s LFP standardisation across GoGo variants, and Luminous Power Technologies’ 500 MWh lithium-ion assembly line (January 2026) signal the accelerating technology transition.

Passenger transport dominates the market with approximately 75–80% of total electric three-wheeler retail, driven by e-rickshaws providing feeder connectivity to mass transit systems and L5 e-autos replacing CNG and diesel auto rickshaws on urban routes. The segment benefits from daily predictable utilisation patterns (80–100 km/day), making TCO calculations straightforward and favourable for electrification.

Electric cargo three-wheelers are the fastest-growing application segment, driven by explosive e-commerce growth, quick-commerce expansion, and fleet electrification mandates from logistics platforms. Borzo launched an e-three-wheeler fleet in Mumbai in January 2025. Amazon and Flipkart are expanding electric last-mile fleets. This application extends to municipal services (solid waste collection, water delivery) and industrial intra-factory transport. For insights into how electric three-wheeler exports may reshape emerging-market mobility, see the Africa Two-Wheeler Market report on Marqstats, which covers motorised transport electrification trends across the continent.

By Geography

North India (Delhi-NCR, Uttar Pradesh, Bihar, Haryana)

North India dominates the India e-rickshaw market, with Delhi-NCR, Uttar Pradesh, Bihar, and Haryana accounting for the largest concentration of e-rickshaw deployments. E-rickshaws serve as primary feeder modes for Delhi Metro, Lucknow Metro, and regional bus networks. Delhi’s Air Pollution Mitigation Plan and CAQM’s clean-fuel mandate (November 2026) further accelerate electric three-wheeler adoption in the NCR. Uttar Pradesh accounts for the highest electric vehicle registrations nationally, with significant e-rickshaw density across Lucknow, Varanasi, Allahabad, and smaller cities. The organised-versus-unorganised transition is most visible in this region, with Bajaj and Mahindra scaling dealer networks to displace local assemblers.

East India (West Bengal, Bihar, Odisha, Jharkhand, Assam)

East India represents a large and price-sensitive e-rickshaw market, with Kolkata, Patna, and Guwahati hosting dense e-rickshaw networks. Lead-acid batteries dominate this region due to cost sensitivity. The transition to lithium-ion is slower here but accelerating as prices decline and financing options expand. The region’s terrain (flat river plains) and climate are well-suited to e-rickshaw operations.

South India (Karnataka, Tamil Nadu, Telangana, Kerala)

South India represents the fastest-growing region for L5 electric auto rickshaws, led by Bengaluru, Chennai, and Hyderabad. Mahindra’s manufacturing hub in Zaheerabad, Telangana anchors the supply side for its electric three-wheeler portfolio. Tamil Nadu’s automotive ecosystem and Karnataka’s EV policy support rapid adoption. Supertech EV commenced operations at its Harapanahalli, Karnataka facility (February 2026) adding 1,200 electric three-wheeler annual capacity.

West India (Maharashtra, Gujarat, Rajasthan)

West India represents growing adoption in both passenger and cargo segments, with Mumbai, Pune, Ahmedabad, and Surat as key markets. Maharashtra’s progressive EV policy and Gujarat’s industrial base support manufacturing. The region leads in electric cargo three-wheeler adoption for e-commerce logistics, driven by Mumbai’s dense urban delivery demand and Pune’s technology startup ecosystem.

How Competition Is Evolving

The India electric three-wheeler market features a distinctive competitive structure: a vast unorganised assembler base (approximately 600 manufacturers on the Vahan portal) coexisting with an increasingly dominant cluster of organised legacy OEMs. Mahindra Last Mile Mobility was recognised as India’s number-one electric commercial vehicle manufacturer for the fourth consecutive year in FY2025, surpassing 300,000 cumulative EV deliveries by November 2025. Its portfolio spans Treo (139 km ARAI-certified range, 7.4 kWh), Treo Plus (167 km ARAI-certified, 10.24 kWh), e-Alfa Plus (e-rickshaw, 100 km range), and cargo variants Zor Grand and Treo Zor. In February 2026, Mahindra launched the UDO electric auto-rickshaw at an introductory price of INR 3,58,999.

Bajaj Auto is the breakout competitor. Having launched the GoGo brand in February 2025 with three passenger variants (P5009, P5012, P7012) offering a best-in-class 251 km certified range and a 5-year battery warranty from INR 3.27 lakh, Bajaj recorded 330% YoY growth in April 2025 (5,509 units). In February 2026, Bajaj launched the WEGO P9018 with a 17.7 kWh battery and 296 km certified range at INR 4,41,247, targeting semi-urban and rural operators. TVS Motor entered in January 2025 with the King EV MAX (179 km certified range, INR 2.95 lakh). Piaggio launched the Ape E-City Ultra in July 2025 with 236 km certified range (approximately 205 km real-world) using LFP chemistry.

In the cargo segment, Euler Motors raised INR 4.38 billion in Series E funding (March 2026) for manufacturing expansion. Omega Seiki Mobility launched the NRG with 300 km certified range (March 2025). Montra Electric (Murugappa Group’s TI Clean Mobility) unveiled the EVIATOR electric small commercial vehicle at Bharat Mobility Expo 2025 with 245 km certified range. Atul Auto announced the acquisition of its subsidiary’s L5 electric three-wheeler business (January 2026) for INR 352.6 million, consolidating its EV portfolio. Legacy e-rickshaw brands including YC Electric, Saera Electric (Mayuri), Kinetic Green, Lohia Auto, and Dilli Electric face growing competitive pressure from these organised OEMs.

Companies Covered

The report profiles 16++ companies with full strategy and financials analysis, including:

Recent Market Activity

Table of Contents

Coverage & Segmentation

This report provides a comprehensive analysis of the India electric three-wheeler market covering 2021–2030, with 2025 as the base year, historical data from 2021 to 2025, and forecast projections from 2026 to 2030. The study examines market size (in USD million and unit volumes), growth trends, competitive landscape, and segment-level forecasts across seven dimensions: by vehicle type (e-rickshaw, L5 passenger, L5 cargo, e-cart), by battery type (lead-acid, lithium-ion LFP, lithium-ion NMC), by motor type (BLDC hub, mid-drive, differential), by power output, by voltage capacity, by driving range, and by region (North, South, East, West India). The analysis covers the complete value chain from battery manufacturing and vehicle assembly through retail, fleet operations, charging infrastructure, and battery swapping networks.

Primary data sources include FADA (Federation of Automobile Dealers Associations) retail data collated with the Ministry of Road Transport & Highways from 1,401–1,459 RTOs (note: Telangana figures are excluded from FADA releases), the Vahan registration portal (a dynamic database where figures may vary by pull date), PM E-DRIVE portal data, and Parliamentary committee notes. Secondary sources include OEM annual reports, investor presentations, industry body publications, trade media, and proprietary primary research with OEMs, fleet operators, battery manufacturers, and charging infrastructure providers. The report profiles 16 electric three-wheeler manufacturers in India covering organised legacy OEMs, emerging EV startups, and infrastructure players.