Market Snapshot

Key Takeaways

Market Overview & Analysis

Report Summary

The non-terrestrial network satellite-cellular integration market encompasses the satellite constellations, ground infrastructure, chipsets, terminals, software platforms, and network integration services that enable seamless connectivity between terrestrial cellular networks and space-based communication systems. The market scope covers LEO, MEO, and GEO satellite architectures, D2D connectivity for smartphones and IoT devices, NTN-specific hardware components (RF front-ends, antennas, onboard processors), and the associated spectrum management and regulatory frameworks. The technology is standardised through 3GPP Releases 17 and 18, with Release 19 expected to further enhance mobility, power efficiency, and broadband capabilities. The study period spans 2021–2030, with 2025 as the base year.

The NTN market represents a paradigm shift in telecommunications architecture. Historically, satellite communications operated as a separate industry from cellular networks, with proprietary protocols, specialised hardware, and premium pricing that limited adoption to maritime, aviation, military, and remote industrial users. The integration of NTN specifications into 3GPP standards fundamentally changes this dynamic by enabling standard 5G smartphones to connect directly to satellites using the same protocols, chipsets, and SIM cards used for terrestrial cellular connectivity. This convergence creates a unified network fabric where handovers between terrestrial and satellite links occur seamlessly, enabling mobile operators to offer ‘coverage everywhere’ as a standard service tier rather than a premium add-on.

The market features two primary competitive approaches. The first involves new-entrant LEO operators like SpaceX (Starlink) and AST SpaceMobile that reuse terrestrial mobile spectrum licensed to MNO partners (T-Mobile, AT&T, Vodafone) to connect existing, unmodified smartphones. The second involves traditional mobile satellite service (MSS) operators like Globalstar (partnered with Apple), Skylo (partnered with Verizon, Google, Samsung, Comcast, Orange), and Sateliot that deploy 3GPP-standardised 5G NTN services on dedicated satellite spectrum. Both approaches are converging toward the same goal—ubiquitous connectivity—but differ in spectrum strategy, business model, and technical architecture. The NTN-Mobile segment alone is estimated to reach nearly USD 18 billion by 2030 with up to 200 million connections.

Market Dynamics

Key Drivers

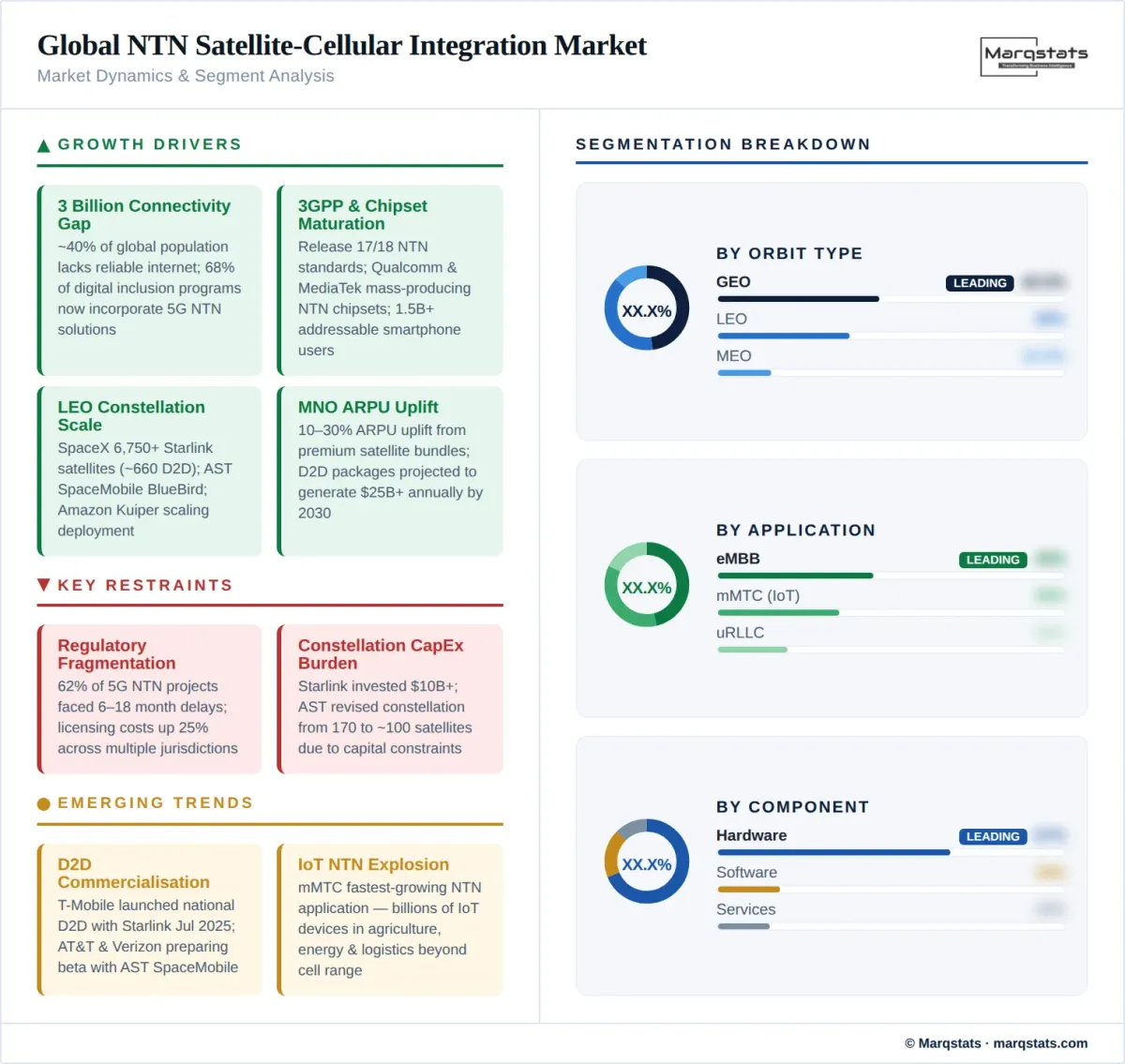

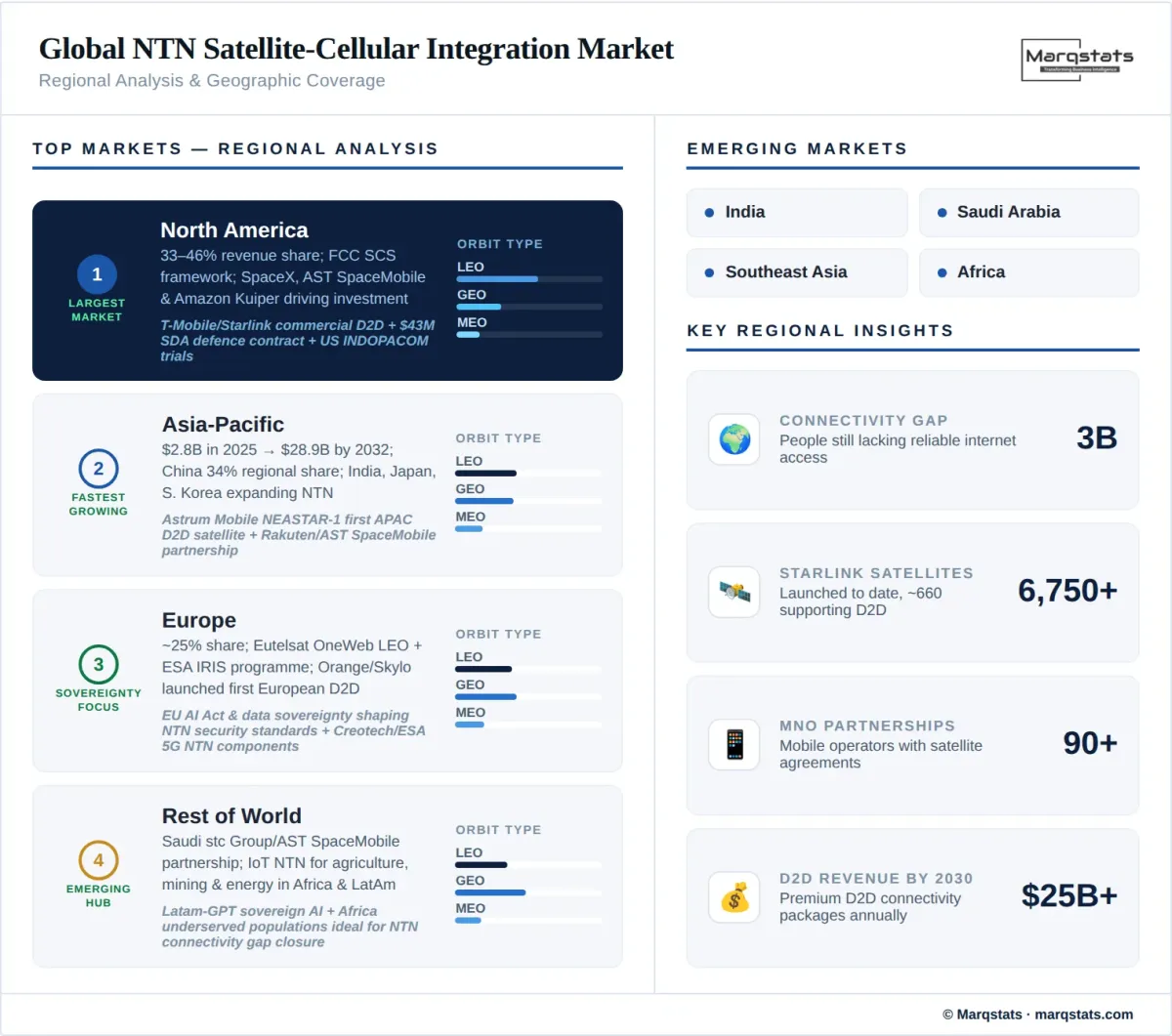

- Global connectivity gap of 3 billion unconnected people: According to GSMA, approximately 40% of the global population still lacks reliable internet access as of 2025, while 5.5 billion people are expected to have mobile internet by 2030. NTN technology is the most cost-effective path to closing this gap in remote, rural, maritime, and mountainous regions where terrestrial infrastructure is economically unfeasible. In 2025, 68% of national digital inclusion programmes incorporated 5G NTN solutions, extending broadband access to 120 million previously unconnected users.

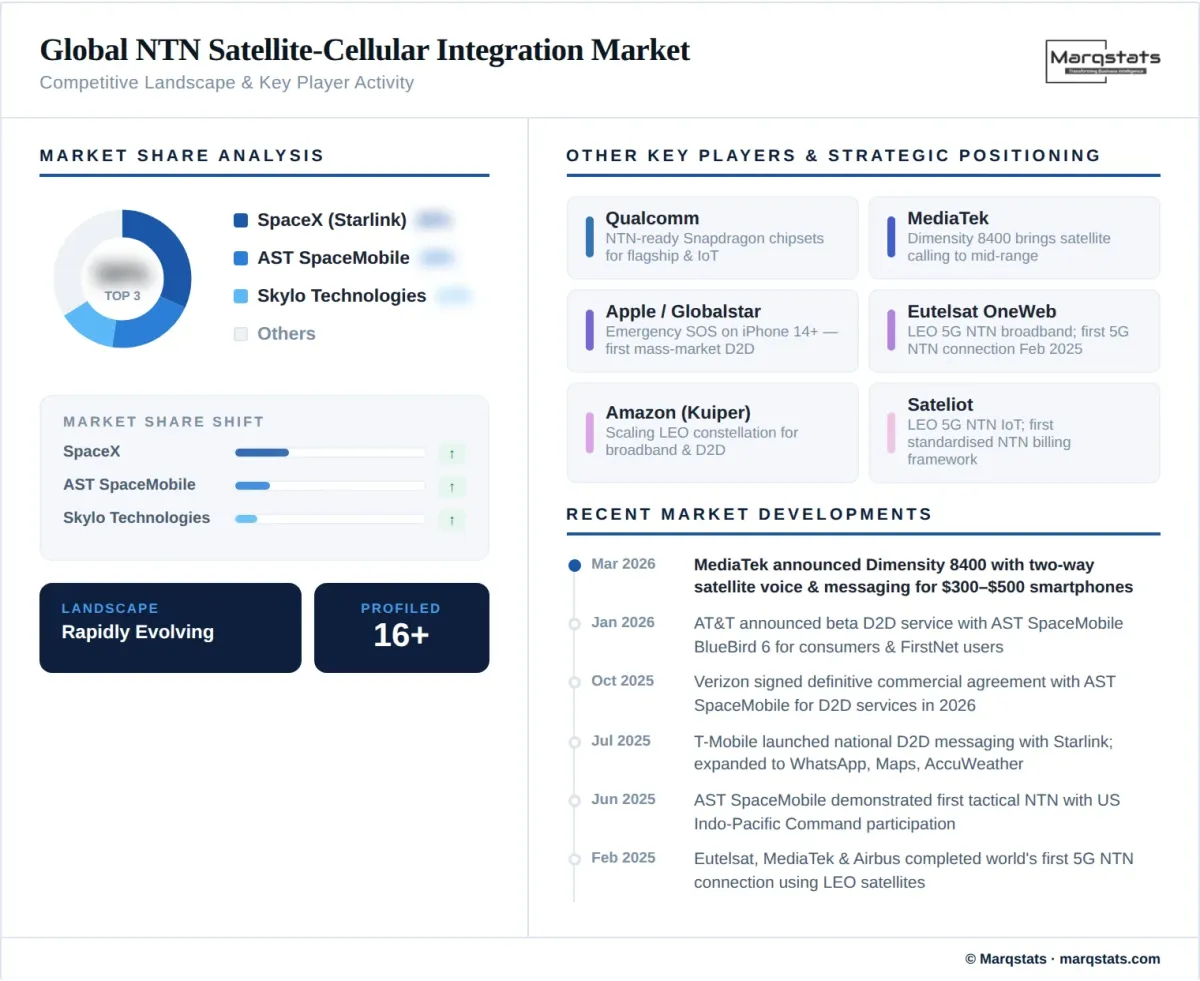

- 3GPP standardisation and chipset ecosystem maturation: 3GPP Release 17 introduced the NTN standard, Release 18 enhances mobility and power efficiency, and Release 19 is in progress. NTN-ready chipsets from Qualcomm and MediaTek are entering mass production, making D2D a standard feature in smartphones and IoT devices. MediaTek’s Dimensity 8400 brings satellite voice calling and messaging to mid-range smartphones ($300–$500), creating an enormous addressable market. Samsung’s Exynos modems integrate 5G NTN capability, and Skylo has certified Qualcomm’s 212S and 9205S modems for satellite IoT.

- Massive LEO constellation deployment reducing cost and latency: SpaceX has launched over 6,750 Starlink satellites, with approximately 660 supporting D2D services. Amazon’s Project Kuiper is scaling its constellation. AST SpaceMobile is deploying BlueBird satellites for broadband D2D. LEO satellites orbit close to Earth (500–2,000 km), enabling latencies of 20–50 ms versus 500+ ms for GEO satellites, making real-time applications like video calls and online gaming feasible over satellite links.

- MNO commercial incentives and ARPU uplift: Early 2025 GSMA Intelligence data indicates a 10–30% ARPU uplift when satellite connectivity is included in premium mobile bundles. Premium D2D connectivity packages are expected to generate over USD 25 billion annually by 2030. T-Mobile’s D2D service with Starlink has expanded beyond messaging to include WhatsApp, Google Maps, and AccuWeather, demonstrating consumer willingness to engage with satellite-enhanced mobile plans.

- Defence and public safety demand for resilient connectivity: Governments are investing in NTN for defence, disaster response, and first-responder communications. AST SpaceMobile demonstrated tactical NTN connectivity with U.S. Indo-Pacific Command, won a USD 43 million Space Development Agency contract, and AT&T plans D2D satellite access for FirstNet public safety users. The military use case for communications in denied or austere environments where terrestrial networks are unavailable or compromised is driving significant government procurement.

Key Restraints

- Regulatory fragmentation and spectrum coordination complexity: 62% of 5G NTN projects in 2025 faced 6–18 month delays due to regulatory approvals and spectrum coordination issues, with average licensing costs increasing by 25% across multiple jurisdictions. Coordinating satellite spectrum with terrestrial mobile operators to prevent interference remains a persistent technical and regulatory challenge, particularly for operators like SpaceX and AST SpaceMobile that reuse MNO spectrum.

- High satellite constellation deployment and maintenance costs: Building and maintaining LEO constellations of hundreds or thousands of satellites requires billions of dollars in capital expenditure. SpaceX’s Starlink has invested over USD 10 billion, while AST SpaceMobile revised its constellation from 170 to approximately 100 satellites. Satellite lifecycle management, orbital debris mitigation, and ground infrastructure costs present significant financial barriers to market entry.

- Latency and quality-of-service variability: Even LEO systems experience variable QoS due to weather conditions, atmospheric interference, and dynamic beam handovers. GEO systems impose 500+ ms latency unsuitable for real-time applications. SAR (specific absorption rate) regulations limit smartphone transmission power, reducing satellite link margins. Until advanced onboard processing and inter-satellite links mature, NTN will complement rather than replace terrestrial 5G for many applications.

- Geopolitical restrictions on satellite communications: Several countries, including China, India, Russia, Cuba, and North Korea, either prohibit or heavily regulate D2D satellite connectivity due to national security, frequency control, or encryption concerns. These restrictions limit the addressable market and complicate global service deployment for satellite operators seeking worldwide coverage.

Key Trends

- Direct-to-Device (D2D) commercialisation accelerating: T-Mobile launched national D2D messaging with Starlink in July 2025, making the service available not only to T-Mobile customers but also to AT&T and Verizon subscribers. AT&T is preparing a beta D2D service with AST SpaceMobile for H1 2026. Verizon signed a definitive commercial agreement with AST SpaceMobile in October 2025. Comcast and Charter Communications partnered with Skylo for D2D messaging on Xfinity Mobile and Spectrum Mobile. Orange launched the first 5G NTN-based D2D service in Europe with Skylo, initially for Google Pixel 9/10 users.

- Hybrid multi-orbit network architectures emerging: Operators are combining LEO (low latency), MEO (balanced coverage), and GEO (wide area) satellites into hybrid constellations to optimise performance across different use cases. OneWeb and Set Network partnered in 2023 for hybrid LEO-GEO connectivity. Intelsat deployed a hybrid NTN solution using GEO-LEO integration for managed enterprise networking. Kymeta unveiled a dual-band antenna in June 2025 for seamless multi-orbit connectivity.

- IoT NTN becoming the highest-volume application: Massive machine-type communications (mMTC) for IoT is projected as the fastest-growing NTN application. Billions of IoT devices in agriculture, energy, logistics, and maritime operate beyond terrestrial coverage. General Dynamics partnered with Skylo in March 2025 for satellite-cellular IoT coverage. Sateliot launched the telecommunications sector’s first standardised billing framework for NTN IoT connectivity with Syniverse in June 2025. Tele2 became the first Swedish operator to offer a commercial 3GPP-based satellite IoT solution.

- Defence sector emerging as a premium NTN vertical: AST SpaceMobile’s tactical NTN demonstration with U.S. Indo-Pacific Command showcased real-time TAK (Tactical Assault Kit) connectivity over standard smartphones. The Defence Innovation Unit awarded AST SpaceMobile and Fairwinds Technologies the Hybrid Space Architecture 2 project. The FCC’s SCS framework supports both commercial and defence applications. Defence NTN use cases include communications in denied environments, maritime surveillance, and disaster response.

Market Segmentation

LEO is the fastest-growing orbital segment at a projected 38.2% CAGR, driven by the massive scale of constellation deployments from SpaceX (6,750+ satellites), AST SpaceMobile, Amazon Project Kuiper, and Eutelsat OneWeb. LEO satellites orbit at 500–2,000 km altitude, providing latencies of 20–50 ms that enable real-time voice, video, and broadband applications. LEO D2D services are the primary focus of the consumer market, with T-Mobile/Starlink and AT&T/AST SpaceMobile partnerships defining the competitive landscape. The lower latency and higher throughput of LEO constellations make them the preferred architecture for broadband NTN services.

GEO held the largest market share at approximately 46.5% in 2024, though this dominance reflects the installed base of legacy satellite infrastructure rather than growth trajectory. GEO satellites provide broad, consistent coverage from a fixed orbital position at approximately 35,786 km altitude, making them suitable for broadcasting, IoT messaging, and maritime/aviation connectivity. Viasat, in collaboration with Skylo, is deploying 5G NTN NB-IoT messaging services via GEO with chipsets from MediaTek, Sony, and Qualcomm. However, 500+ ms latency limits GEO’s suitability for real-time consumer applications.

MEO satellites operate at 2,000–35,786 km altitude, offering a balance between LEO’s low latency and GEO’s wide coverage. MEO constellations like SES’s O3b mPOWER are deployed for enterprise-grade managed services, maritime broadband, and government communications. While MEO represents a smaller market share than LEO or GEO, it plays a critical role in hybrid multi-orbit architectures where different orbital layers are combined to optimise service quality across diverse use cases.

eMBB is the marquee consumer application for NTN, enabling smartphone users to access broadband internet, video calling, and app-based services in areas without terrestrial cellular coverage. AST SpaceMobile’s BlueBird satellites demonstrated D2D video calls on standard smartphones using AT&T and Verizon spectrum. T-Mobile’s Starlink D2D service has expanded from basic messaging to full app support. The eMBB segment is driven by the 1.5+ billion smartphone users in areas with partial or no terrestrial coverage.

mMTC is the fastest-growing application segment, driven by the explosion of IoT devices in agriculture, energy, logistics, maritime, and infrastructure monitoring. These devices require low-power, low-data-rate connectivity over vast geographic areas where terrestrial networks are unavailable. Skylo, Sateliot, and Myriota are leading mMTC NTN deployments. General Dynamics partnered with Skylo in March 2025 for satellite-cellular IoT. The NB-IoT NTN standard enables existing IoT chipsets to connect to satellites with minimal hardware modifications.

uRLLC applications for NTN include defence tactical communications, disaster response coordination, maritime safety, and autonomous vehicle connectivity. These applications demand high reliability and minimal latency, which currently favours LEO constellations with advanced onboard processing. AST SpaceMobile’s tactical NTN demonstration with U.S. military participation showcased real-time data, voice, and video on unmodified smartphones, validating the defence uRLLC use case.

By Geography

North America

North America dominates the NTN market with approximately 33–46% revenue share, anchored by the United States where the 5G NTN market alone was valued at approximately USD 3.82 billion in 2025. The region benefits from the world’s largest LEO constellation operators (SpaceX, AST SpaceMobile, Amazon), the FCC’s SCS regulatory framework, and early commercial D2D launches by T-Mobile. The U.S. defence sector provides additional demand through Space Development Agency contracts and USINDOPACOM trials. SpaceX’s Starlink D2D constellation (approximately 660 satellites) and Amazon’s Project Kuiper represent multi-billion-dollar investment commitments anchoring long-term growth.

Europe

Europe accounts for approximately 25% of the satellite NTN market in 2025. The region’s growth is driven by Eutelsat OneWeb’s LEO constellation, the European Space Agency’s IRIS programme (which will leverage 5G NTN for satellite-terrestrial interoperability), and Orange’s commercial D2D launch with Skylo. The EU Cyber Resilience Act and data sovereignty requirements are shaping security standards for NTN deployments. In January 2025, Creotech Instruments signed a deal with ESA to develop 5G NTN integration components for private mmWave 5G networks. Eutelsat, MediaTek, and Airbus completed the first 5G NTN connection using LEO satellites in February 2025.

Asia-Pacific

Asia-Pacific is projected as the fastest-growing region, valued at approximately USD 2.80 billion in 2025 and projected to reach USD 28.90 billion by 2032. China accounts for the largest regional share at approximately 34% driven by state-backed satellite programmes. India, Japan, South Korea, and Southeast Asia are expanding NTN adoption for rural connectivity, maritime monitoring, and disaster response. Singapore-based Astrum Mobile selected SWISSto12 to produce NEASTAR-1, the first dedicated satellite-to-device platform in Asia-Pacific for 5G NTN services. Japan’s Rakuten is an AST SpaceMobile strategic partner.

Rest of World

Latin America, the Middle East, and Africa represent emerging NTN markets with significant potential for satellite-enabled connectivity. These regions contain large underserved populations where terrestrial network economics are unfavourable, making NTN the primary viable path to connectivity. Saudi Arabia’s stc Group is an AST SpaceMobile strategic partner. African and Latin American markets are particularly attractive for IoT NTN applications in agriculture, mining, and energy, where remote asset monitoring over satellite networks creates high-value use cases.

How Competition Is Evolving

The NTN satellite-cellular integration market features a complex competitive ecosystem spanning satellite constellation operators, chipset manufacturers, mobile network operators, and ground infrastructure providers. The market is bifurcated between new-entrant D2D operators and traditional mobile satellite service providers. SpaceX’s Starlink leads in constellation scale with over 6,750 satellites and approximately 660 dedicated D2D satellites, partnered with T-Mobile for the first commercial national D2D service. AST SpaceMobile is the only publicly traded pure-play D2D satellite company (NASDAQ: ASTS), with strategic partnerships spanning AT&T, Verizon, Vodafone, American Tower, Bell, Google, Rakuten, and stc Group—agreements with 50 mobile operators worldwide.

On the MSS/standardised NTN side, Skylo Technologies has emerged as a pivotal player, partnering with Verizon, Google, Samsung, Comcast, Charter, Orange, and Tele2 to deliver 3GPP-based NTN services. Skylo has certified Qualcomm and MediaTek modems for its network and partnered with Murata for dual TN/NTN modules. Globalstar’s partnership with Apple (emergency SOS on iPhone 14+) established the first mass-market satellite-phone integration. Sateliot is deploying LEO-based 5G NTN IoT services with the first standardised NTN billing framework via Syniverse. Eutelsat OneWeb is positioning its LEO constellation for 5G NTN broadband with the IRIS programme.

The chipset layer is dominated by Qualcomm and MediaTek, who are integrating NTN capabilities into mainstream 5G System-on-Chip platforms. MediaTek’s Dimensity 8400 brings satellite calling to mid-range smartphones, while Qualcomm’s Snapdragon platforms support NTN across flagship and IoT segments. Samsung’s Exynos modems incorporate 5G NTN capability. On the antenna and hardware front, Kymeta’s dual-band multi-orbit antenna and Airbus Defence and Space’s satellite platforms are key enablers. The market is expected to consolidate as spectrum acquisitions (SpaceX’s USD 17 billion spectrum deal) and mergers (Lynk/Omnispace) reshape the competitive landscape.

Companies Covered

The report profiles 16+ companies with full strategy and financials analysis, including:

Recent Market Activity

Table of Contents

Coverage & Segmentation

This report provides a comprehensive analysis of the global non-terrestrial network satellite-cellular integration market covering the period 2021–2030, with 2025 as the base year, historical data from 2021 to 2025, and forecast projections from 2026 to 2030. The study examines market size in USD billion, growth trends, competitive landscape, and segment-level forecasts by orbit type (LEO, MEO, GEO), technology (NR NTN, IoT NTN), frequency band (L, S, C, Ku/Ka, HF/VHF/UHF), application (eMBB, mMTC, uRLLC), end-use sector (commercial, defence, government), component (hardware, software, services), and region.

The analysis covers the complete NTN ecosystem from satellite constellation operators and chipset manufacturers through mobile network operator partnerships, ground infrastructure providers, and regulatory frameworks. Competitive profiling spans 16 companies. The report provides strategic guidance on MNO satellite partnership evaluation, D2D service launch planning, spectrum strategy assessment, and investment prioritisation for enterprises and investors evaluating the NTN opportunity.