Market Snapshot

Key Takeaways

Market Overview & Analysis

Report Summary

The global sensor market encompasses all electronic and electromechanical devices that detect, measure, and convert physical, chemical, biological, and environmental phenomena into electrical signals for processing, analysis, and actuation. The market scope covers the full spectrum of sensor technologies including MEMS (accelerometers, gyroscopes, pressure sensors, microphones), CMOS image sensors, optical and photonic sensors, LiDAR and radar, temperature and humidity sensors, gas and chemical sensors, biosensors, force and torque sensors, position and proximity sensors, flow sensors, and emerging quantum sensors. The study period spans 2021–2030, with 2025 as the base year.

Sensors are the foundational hardware layer of the digital economy. There were approximately 30 billion network-connected devices and connections globally by end of 2023, up from 18.4 billion in 2018, and this number is projected to exceed 40 billion by 2030. Every connected device relies on one or more sensors for environmental awareness. The automotive industry alone consumed approximately USD 40 billion in sensors in 2024, with modern vehicles containing 100–200+ sensors spanning inertial measurement units, LiDAR arrays, radar modules, camera systems, tire pressure monitors, battery management sensors, and cabin occupancy detectors. The healthcare sector is experiencing a sensor revolution as continuous glucose monitors, cuff-less blood-pressure wearables, pulse oximeters, and lab-on-chip diagnostics move from clinical settings to consumer wearables.

The market is entering a new innovation cycle driven by three technology inflections. First, the convergence of AI and sensor hardware is creating ‘smart sensors’ capable of running inference models at the edge—Bosch’s BMI323 six-axis IMU with an on-chip machine-learning core and Bosch’s BMA530 accelerometer with an integrated ML core that cuts system power by 40% in wearables exemplify this trend. Second, the transition to 300 mm MEMS wafer manufacturing (STMicroelectronics inaugurated a 300 mm MEMS line in Italy with 10,000 wafers per month capacity in October 2025) is reducing per-die cost by 30–40% and enabling economies of scale for automotive and consumer applications. Third, ‘sensor fusion’—the AI-driven blending of data from multiple sensor modalities (radar, camera, LiDAR, ultrasonic) into unified perception models—is becoming the standard architecture for autonomous vehicles, robotics, and smart factory systems. The sensor fusion market alone is projected to grow from USD 8.0 billion in 2025 to USD 75.5 billion by 2035 at a 24.7% CAGR.

Market Dynamics

Key Drivers

- IoT proliferation and connected device explosion: The number of connected IoT devices is projected to reach 40 billion by 2030. Every endpoint—from factory machinery and logistics assets to wearable health monitors and smart home appliances—requires one or more sensors for environmental awareness, condition monitoring, and data capture. The industrial IoT (IIoT) segment is driving demand for ruggedised temperature, pressure, vibration, and flow sensors that enable predictive maintenance, cutting unplanned factory downtime by up to 50%.

- Automotive sensor content escalation and ADAS mandates: The EU General Safety Regulation 2019/2144 requires automatic emergency braking, lane departure alerts, and driver monitoring systems on every new model by 2026, establishing a floor of vision, radar, and ultrasonic hardware per vehicle. Modern ADAS-equipped vehicles contain 100–200+ sensors. The EV transition adds battery management sensors (current, temperature, voltage) and thermal monitoring. LiDAR and radar for Level 3+ autonomy represent the highest-growth automotive sensor segments.

- Industry 4.0 and smart manufacturing transformation: Manufacturing facilities are deploying massive sensor networks for real-time process control, quality inspection, and predictive maintenance. Edge-AI sensor clusters enable local inference without cloud latency. Smart factories use vibration sensors for machine health monitoring, vision systems for defect detection, and gas sensors for safety compliance. Germany’s discrete-manufacturing sector deploys AI-enabled MEMS modules to cut scrap rates.

- Wearable health monitoring and medical diagnostics growth: The medical and wellness sensor segment is forecast to grow at 11.98% CAGR through 2031—the fastest among end-user verticals. Biocompatible MEMS pressure and biochemical sensors enable continuous glucose monitors and cuff-less blood-pressure wearables. Lab-on-chip diagnostics bring point-of-care testing outside clinical settings. FDA 510(k) pathways enable 12-month commercialisation cycles for medical MEMS devices.

- AI integration transforming sensors into edge intelligence nodes: The convergence of AI co-processors with sensor front-ends is creating intelligent sensors that process data locally rather than transmitting raw data to the cloud. Bosch integrates AI co-processors inside its latest MEMS devices. Infineon’s SURF (Sensor Units & Radio Frequency) business unit merges sensor and RF capabilities for ambient IoT and green-energy markets. Honeywell partnered with Qualcomm on AI-powered industrial sensor solutions. This trend reduces bandwidth requirements, improves latency, and enhances privacy for sensitive applications.

Key Restraints

- Supply chain constraints and foundry capacity limitations: Tight 200 mm MEMS foundry capacity constrains production for legacy sensor designs. AEC-Q100 automotive qualification cycles span up to two years, and only a few Asia-Pacific fabs meet stringent automotive criteria. While the transition to 300 mm wafers is underway, capital expenditure requirements remain high—STMicroelectronics invested EUR 200 million to expand its Agrate Brianza MEMS fab.

- High integration costs for automotive-grade LiDAR: The cost of integrating premium LiDAR components into mid-range vehicles remains a barrier to mass adoption. While solid-state and MEMS-based LiDAR solutions are reducing costs, achieving the sub-USD 500 price point required for mass-market deployment remains challenging. This limits the addressable market for autonomous driving sensor stacks beyond premium vehicle segments.

- Calibration drift in long-lifecycle industrial sensors: Sensors deployed on offshore wind turbines, oil platforms, and critical infrastructure must remain accurate for 10–20 years without human access. Calibration drift in vibration, pressure, and chemical sensors compromises long-term reliability and increases total cost of ownership for industrial applications.

- Cybersecurity risks in wireless sensor networks: The proliferation of IoT-connected sensors creates expanded attack surfaces. The EU Cyber Resilience Act compels suppliers to certify software-driven sensors, increasing design complexity. Securing wireless sensor data streams from edge to cloud while maintaining low power consumption and latency remains an engineering challenge.

Key Trends

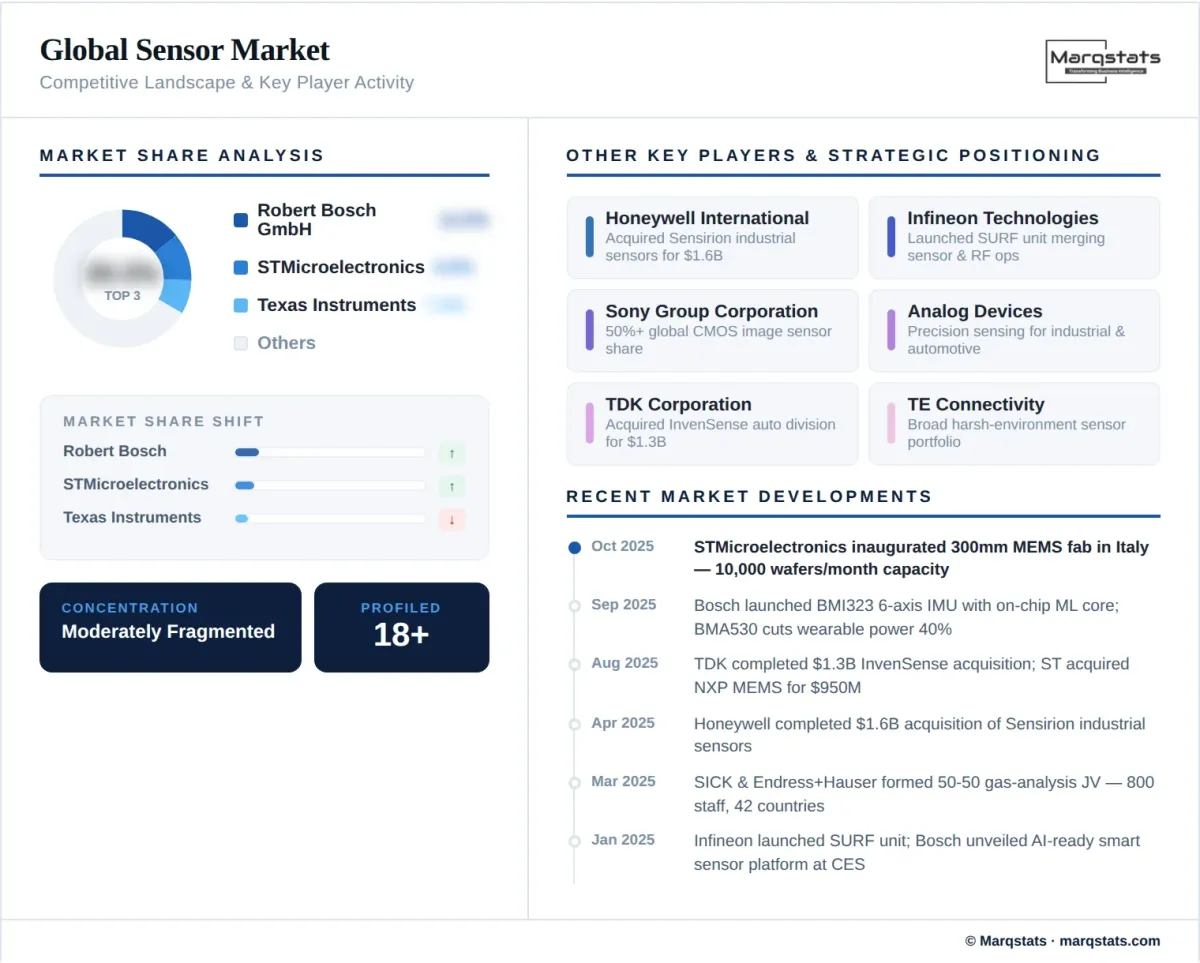

- MEMS industry consolidation and M&A wave: The sensor market is experiencing unprecedented consolidation. STMicroelectronics acquired NXP’s MEMS sensor business for USD 950 million to strengthen its automotive inertial sensor position. TDK acquired InvenSense’s automotive sensor division for USD 1.3 billion. Honeywell completed the USD 1.6 billion acquisition of Sensirion’s industrial sensors. Syntiant purchased Knowles’ consumer MEMS microphone division for USD 150 million. Viavi acquired Inertial Labs for USD 150 million for aerospace and defence exposure. Bosch announced a USD 270 million venture fund targeting deep-tech sensor startups.

- Photonics-MEMS fusion and optical MEMS growth: Optical MEMS is expanding at 10.53% CAGR through 2031, driven by LiDAR scanners for autonomous vehicles, micro-mirror arrays for augmented-reality headsets, and silicon photonics integration. AMS-OSRAM shipped the first AEC-Q102-qualified 8-channel LiDAR laser. MicroVision’s 100 Hz beam-steer micro-mirror assembly enables centimetre-level object detection at 200 metres for Level 3 autonomy.

- Quantum sensors entering commercial applications: The quantum sensor market is projected to grow from USD 170.56 million in 2025 to USD 1.34 billion by 2034 at 25.7% CAGR. Quantum sensors offer orders-of-magnitude improvements in sensitivity for magnetic field detection, navigation, and medical imaging. Infineon’s graphene-based Hall-effect device achieves 100x sensitivity over silicon peers, unlocking ultra-low-field detection for robotics applications.

- Sensor fusion becoming the standard perception architecture: The sensor fusion market is projected to grow from USD 8.0 billion in 2025 to USD 75.5 billion by 2035 at 24.7% CAGR. AI-driven fusion of radar, camera, LiDAR, and ultrasonic streams into unified 3D environmental models is becoming the default architecture for autonomous vehicles, collaborative robots, and smart infrastructure. Multi-modal sensor packages that deliver ranging and orientation data from a single socket are replacing discrete sensor deployments.

Market Segmentation

Image sensors command approximately 54% of the sensor market by type in 2025, driven by ubiquitous deployment in smartphones (1.5+ billion units annually), automotive cameras (ADAS, surround-view, in-cabin monitoring), surveillance systems, and medical imaging. Sony dominates the CMOS image sensor segment with over 50% global market share. The segment is evolving toward higher resolution, wider dynamic range, and event-driven (neuromorphic) architectures that reduce power consumption and enable always-on visual intelligence for edge AI applications.

Pressure sensors represent a foundational segment with broad applications across automotive (tire pressure monitoring, engine management), industrial process control, HVAC, medical devices (blood pressure, ventilator monitoring), and aerospace. The segment benefits from mature MEMS manufacturing processes and steady demand growth driven by regulatory mandates and industrial automation expansion.

Accelerometers and speed/motion sensors account for approximately 46% share by type in 2025 when measured by unit volume, driven by smartphones, wearables, automotive stability control, and industrial vibration monitoring. Bosch Sensortec’s BMI323 six-axis IMU with on-chip machine learning and the BMA530 accelerometer with integrated ML core represent the cutting edge of smart inertial sensing. MEMS motion sensor sales reached 7.05 billion units in 2025 at an average price of approximately USD 0.60 per unit.

MEMS technology accounts for approximately 40% of total sensor market revenue in 2025, anchoring the market through cost-effective wafer-level packaging. STMicroelectronics alone ships more than 2 billion capacitive accelerometers and gyroscopes annually for smartphones, automobiles, and industrial robots. The MEMS sensor market is valued at USD 18.61 billion in 2025, growing to USD 29.08 billion by 2031 at 8.03% CAGR. The transition to 300 mm substrates is critical for meeting automotive and smartphone volumes while reducing per-die cost by 30–40%.

CMOS technology underpins the image sensor segment and is the dominant platform for high-volume consumer and automotive imaging applications. While CMOS imagers are approaching saturation in mature smartphone segments, they remain core to dash-cam, security camera, and automotive ADAS refresh cycles. Advanced stacked CMOS architectures enable higher frame rates, improved low-light performance, and on-chip AI processing.

Optical sensing technologies, led by LiDAR, structured-light systems, and fibre-optic sensors, are growing at approximately 26% annually. Optical MEMS is the fastest-growing technology sub-segment at 10.53% CAGR through 2031, driven by autonomous vehicle perception systems and AR/VR display applications. Silicon photonics foundries are integrating optical MEMS scanners with laser drivers and signal-processing chips on single substrates for cost and performance optimisation.

Automotive is the largest end-user vertical at approximately 24.5% of sensor market revenue in 2025. The automotive sensor market was valued at approximately USD 40 billion in 2024, projected to reach USD 88 billion by 2034 at 8.16% CAGR. The EU’s mandatory ADAS requirements by 2026 establish a floor of sensor hardware per vehicle. EV proliferation adds battery-management and thermal-monitoring sensor loads. LiDAR and thermal imaging sensors are projected to represent 26% of automotive sensor revenue by 2036.

Consumer electronics leads by revenue share in 2025 when smartphones, wearables, smart home devices, and gaming consoles are combined. The global smartphone market exceeds 1.5 billion units annually, each containing multiple MEMS sensors (accelerometers, gyroscopes, proximity, ambient light, barometric pressure). Wearable devices are driving demand for biosensors (heart rate, SpO2, continuous glucose) and advanced motion sensors for activity tracking and gesture recognition.

Industrial applications include process automation, predictive maintenance, environmental monitoring, and quality control. The industrial sensors market was valued at USD 30.52 billion in 2025, projected to reach USD 70.5 billion by 2035 at 8.73% CAGR. AI-enabled sensor clusters for Industry 4.0 applications cut unplanned factory downtime by up to 50%. The oil and gas, pharmaceutical, chemical, and energy sectors are major consumers of ruggedised pressure, temperature, flow, and gas sensors.

Healthcare is the fastest-growing end-user vertical at 11.98% CAGR through 2031. Continuous glucose monitors, lab-on-chip diagnostics, cuff-less blood-pressure wearables, and surgical robotics sensors are driving the expansion. Biocompatible MEMS pressure and biochemical sensors enable non-invasive monitoring. The FDA’s 510(k) pathway enables 12-month commercialisation for medical MEMS, accelerating revenue realisation compared to traditional medical device timelines.

By Geography

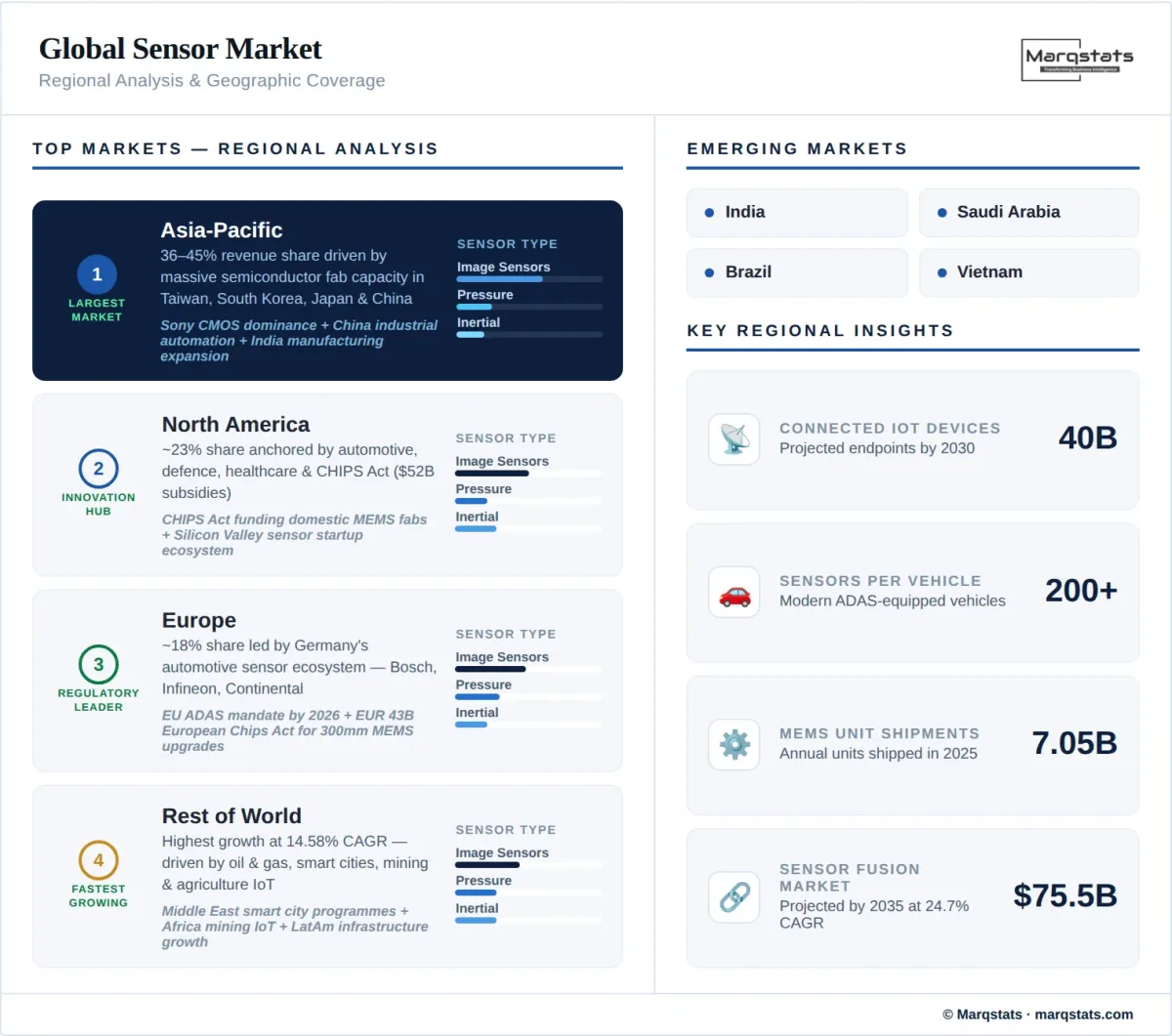

Asia-Pacific

Asia-Pacific dominates the global sensor market with approximately 36–45% revenue share in 2025, driven by massive semiconductor fabrication capacity in Taiwan, South Korea, Japan, and China, along with high-volume consumer electronics assembly and rapidly growing automotive manufacturing. Japan’s Sony dominates CMOS image sensors globally. China’s industrial automation drive and India’s manufacturing expansion are creating strong demand for industrial and automotive sensors. The region hosts the world’s largest MEMS foundries and benefits from lower manufacturing costs and proximity to end-market assembly.

North America

North America holds the second-largest market position at approximately 23% share, anchored by automotive, defence, healthcare, and advanced manufacturing clusters. The CHIPS Act allocates USD 52 billion including provisions for domestic MEMS fabrication. Texas Instruments, Honeywell, Analog Devices, and Broadcom are headquartered in the region. The U.S. defence sector demands high-precision inertial navigation, infrared imaging, and CBRN detection sensors. Silicon Valley and Boston remain global centres for sensor startup innovation, with hundreds of MEMS-related startups attracting eight- and nine-figure funding rounds.

Europe

Europe accounts for approximately 18% market share, led by Germany’s automotive sensor ecosystem anchored by Bosch, Infineon, and Continental. The EUR 43 billion European Chips Act funds 300 mm MEMS wafer upgrades at facilities like X-FAB. STMicroelectronics (France/Italy) supplies multi-sensor modules globally. The EU General Safety Regulation mandating ADAS by 2026 and the Cyber Resilience Act requiring certified software-driven sensors create regulatory demand drivers unique to the region. The UK’s Cambridge cluster incubates optical MEMS startups for LiDAR and AR applications.

Rest of World

Latin America, the Middle East, and Africa represent emerging sensor markets driven by oil and gas instrumentation, infrastructure development, and expanding automotive assembly. The Middle East’s smart city initiatives and industrial diversification programmes create demand for environmental monitoring, building automation, and security sensors. Africa’s mining and agricultural sectors are early adopters of IoT-connected remote monitoring sensors. Overall, the region is expected to register the highest growth rate at 14.58% CAGR through 2031.

How Competition Is Evolving

The global sensor market is moderately fragmented, with diversified semiconductor conglomerates competing alongside specialist niche players. Bosch, STMicroelectronics, and Texas Instruments together supplied approximately 29.3% of global unit shipments in 2025. Bosch remains the number-one MEMS vendor with approximately USD 2 billion in MEMS revenue for 2024, while STMicroelectronics is aggressively expanding through acquisitions—its USD 950 million acquisition of NXP’s MEMS sensor business aims to catapult it into a stronger position in automotive safety sensors. Sony dominates CMOS image sensors with over 50% global share, while Infineon leads in radar and power sensors for automotive electrification.

The market is experiencing an unprecedented M&A consolidation cycle. Beyond the headline acquisitions (ST-NXP USD 950M, TDK-InvenSense USD 1.3B, Honeywell-Sensirion USD 1.6B), secondary deals include Syntiant’s acquisition of Knowles’ consumer MEMS microphone division (USD 150M), Viavi’s acquisition of Inertial Labs (USD 150M) for aerospace and defence, and Qorvo’s USD 125 million acquisition of Nextivity’s RF-repeater business integrating MEMS-based tunable filters. Bosch announced a new USD 270 million venture fund aimed at deep-tech sensor startups, signalling sustained investment appetite. SICK spun its gas-analysis unit into a 50-50 joint venture with Endress+Hauser, pooling 800 staff across 42 countries for decarbonisation instrumentation.

Specialist leaders maintain dominant positions in specific verticals: Sony (image sensors), Velodyne and Ouster (LiDAR), SICK and Endress+Hauser (industrial flow and gas analysis), ams-OSRAM (optical sensing and LiDAR lasers), and Knowles/xMEMS (MEMS microphones and speakers). The competitive landscape is evolving from pure hardware competition toward integrated hardware-software platforms, as AI-enabled sensors with on-chip inference capabilities command premium pricing and create switching costs. Heterogeneous integration—co-packaging MEMS, optical, and ASIC dies into single modules—is becoming a key competitive differentiator.

Companies Covered

The report profiles 18+ companies with full strategy and financials analysis, including:

Recent Market Activity

Table of Contents

Coverage & Segmentation

This report provides a comprehensive analysis of the global sensor market covering the period 2021–2030, with 2025 as the base year, historical data from 2021 to 2025, and forecast projections from 2026 to 2030. The study examines market size in USD billion, growth trends, competitive landscape, and segment-level forecasts by sensor type (image, pressure, inertial, temperature, gas, biosensor, proximity, flow, force, others), technology (MEMS, CMOS, optical/photonic, quantum, NEMS), end-user industry (automotive, consumer electronics, industrial, healthcare, aerospace and defence, energy, others), integration level (discrete, embedded/smart), output (analog, digital), and region.

The analysis covers the complete sensor value chain from semiconductor materials and MEMS foundries through sensor design, packaging, calibration, and system integration. Competitive profiling spans 18 companies covering diversified conglomerates and specialist niche leaders. The report provides strategic guidance on technology selection, sensor fusion architecture evaluation, M&A opportunity assessment, and investment prioritisation for enterprises, semiconductor vendors, and investors navigating the sensor market.