Executive Insight

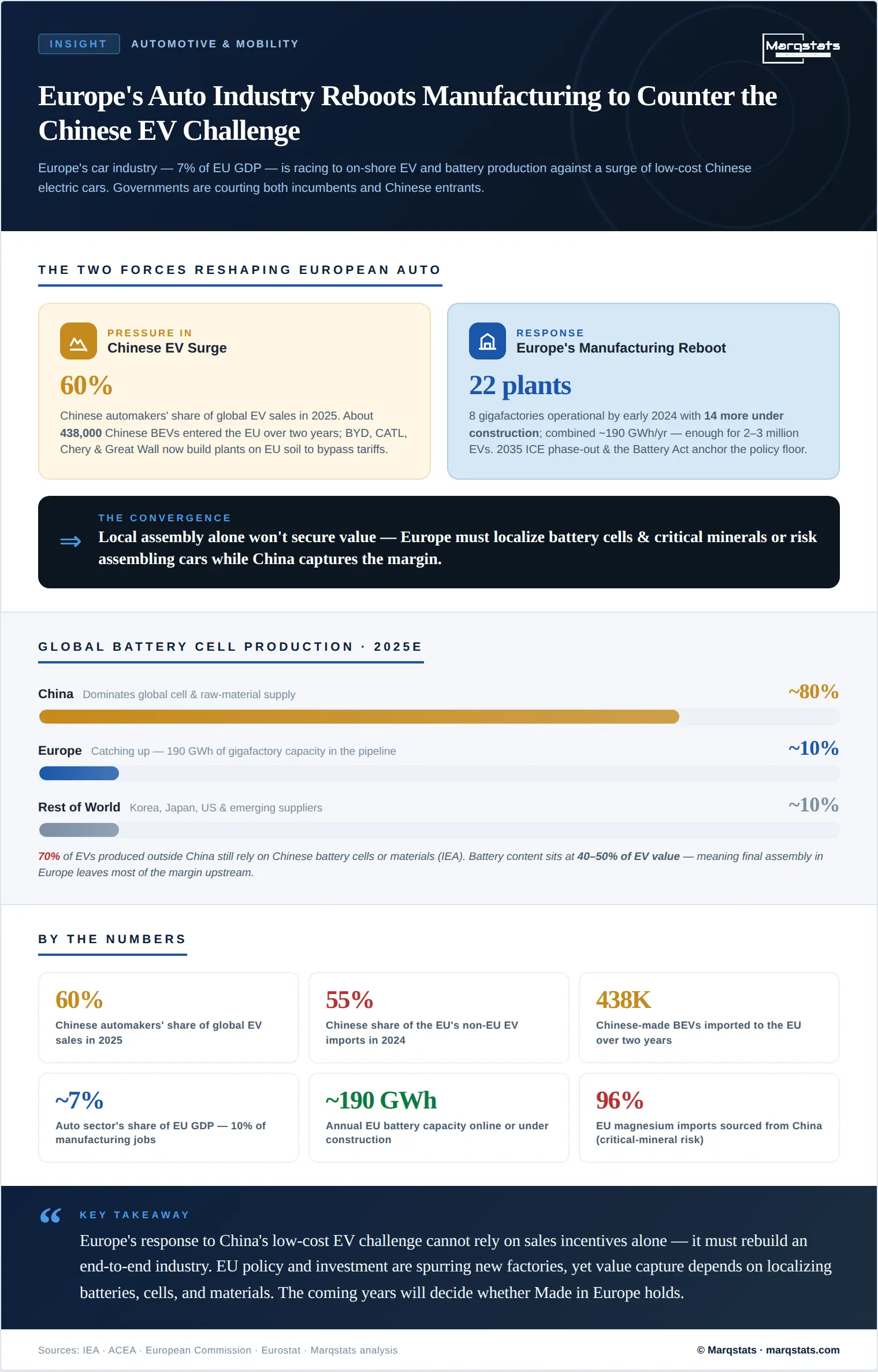

Europe's automakers and battery suppliers are expanding domestic EV capacity quickly to defend against a flood of cheaper Chinese electric vehicles. Over two years, European Union imports of Chinese-made battery EVs rose to about 438,000 units, near 20 percent of the EU market in 2023, even as Chinese brands begin building their own EU plants. Incumbent European OEMs, including Volkswagen, Stellantis, and BMW, have responded with new EV and battery projects, often backed by national subsidies. European Union policymakers, in turn, propose Made-in-Europe rules and tariffs to level the field.

Chinese entrants are adapting rather than retreating. Producing within Europe lets their cars be perceived as European and sidesteps potential duties. Governments from Hungary to Spain are offering cash and tax breaks to attract projects from BYD, CATL, Chery, and others. These factory commitments carry large stakes for jobs and value capture; the auto sector accounts for about 7 percent of EU GDP and 10 percent of manufacturing employment.

Market Context

Global EV sales continue to climb, with the International Energy Agency projecting about 23 million in 2026, though the centre of gravity sits in China. Chinese firms supply roughly 60 percent of global EV sales, supported by deep battery capacity; China is set to produce more than 80 percent of batteries in 2025. Price competition is intense. An average battery EV in China can undercut an equivalent combustion car, whereas EVs in Europe still carry a cost premium.

Europe's own EV output is rising. About EUR 122 billion of EU car production was electric or hybrid in 2024, near 32 percent of cars by units. A heavy share of demand is met by imports; about 20 percent of EU battery-EV sales were Chinese imports in 2023, and 55 percent of non-EU EV imports came from China in 2024. The EU's relatively open market and generous EV subsidies have aided this inflow, in contrast to the United States, which restricts imports through tax-credit conditions.

European capacity is expanding. Eight gigafactories were operational by early 2024, with 14 more under construction, together set to deliver about 190 GWh per year, enough for two to three million cars. Scale and supply chains still trail China. Most battery raw materials must be imported; the EU sources about 96 percent of its magnesium and 38 percent of its natural graphite from China, and China dominates cell production.

European Union climate rules, including the 2035 combustion-engine phase-out, and new trade measures such as the tariff probe on Chinese EVs have created urgency. EU industrial strategy now targets EV and battery sectors directly through instruments such as the Battery Act and major projects of common European interest. National governments use incentives to retain or attract factories.

What Is Changing, and Why Now

Chinese EV output, near 10 million units in 2025, is growing rapidly. A saturated home market and overcapacity push Chinese firms to export and build abroad. Key battery components and raw materials remain largely outside Europe; the International Energy Agency notes that 70 percent of EVs produced outside China rely on Chinese battery cells or materials, so Europe imports much of the value, with battery content estimated at 40 to 50 percent of EV value.

Several forces converge now. Chinese firms aim to secure market share before EU tariffs or local-content rules take effect, and EU EV adoption is accelerating, with nearly 30 percent of EU car sales electric in early 2026. The United States and the European Union increasingly treat EV supply chains as strategic for energy security, while Chinese subsidy phase-outs push exports higher. Without a United States-style incentive package, EU investment risks lagging; assessments suggest a significant share of planned EU battery capacity is at risk from underinvestment.

Who Benefits and Who Is Exposed

European OEMs and suppliers stand to secure production and protect jobs through new EV plants and state-aided battery alliances, such as the Stellantis, Mercedes-Benz, and TotalEnergies joint venture in Italy. Local assembly offers some protection against tariffs, though high energy and labour costs pressure margins. Chinese companies, including BYD, CATL, and Great Wall, gain market access and lower shipping costs by producing within the EU; BYD is building plants in Hungary, and CATL is constructing a 100 GWh facility there, allowing imports to bypass duties. Investors face new opportunities in battery and mining ventures, alongside risk of delays and cost overruns, as Northvolt's setbacks illustrate. Policymakers and consumers weigh cleaner air and technology leadership against trade tensions; consumers benefit from lower EV prices via imports, yet risk fewer choices should EU producers fall behind.

Competitive Landscape

European OEMs are converting plants to EVs at pace. Stellantis's Automotive Cells Company will rebuild Termoli, Italy into a 120 GWh battery plant by 2030, and Volkswagen's battery partnerships target more than 100 GWh of capacity, though some projects have paused amid slower demand. Among Chinese brands, BYD has advanced furthest into Europe with car and bus plants in Hungary, the first Chinese EV manufacturer on the ground; MG, owned by SAIC, imports Chinese-built models, Chery began production in Spain in 2024, and Great Wall is in talks for a Polish factory. Chinese automakers often partner with local firms, such as Leapmotor with Stellantis in Poland.

Among battery suppliers, established European projects from Northvolt and Verkor have faced cost and financing strain, whereas Chinese giants press forward; CATL's Debrecen plant in Hungary and SK On's Hungarian expansion will lift EU output materially. Most new projects are joint ventures with auto OEMs. Component and raw-material supply remains the weak point; Europe holds little domestic cobalt or nickel production and depends on Africa and China for battery-grade minerals. Announced projects exceeding 300 GWh may meet a meaningful share of EU battery demand, yet upstream value capture stays low, since cell production and raw materials remain China-dominated while final assembly sits in Europe.

Scenarios to 2030

Two diverging paths are possible. In a catch-up-and-scale scenario, continued EU support brings dozens of gigafactories online, reaching 100 to 300 GWh by 2030, local raw-material projects come on stream, and a European battery ecosystem forms. Assembly shifts in-house, EU market share holds even as tariffs curb imports, and EV prices converge with combustion cars through scale. European automakers and suppliers prosper.

In a continued-dependency scenario, persistent cost gaps and slow deployment keep many OEMs sourcing EVs and cells from China or trusted partners. Tariffs restrict some imports without removing China's presence, as Chinese joint-venture plants in Eastern Europe expand. Europe's battery ambitions fall short, echoing Northvolt-style failures, leaving the EU a net consumer. EV uptake still grows on policy support, yet much value accrues to Chinese companies, weakening European automotive capital and technology leadership.

Key catalysts include EU policy outcomes, progress on critical minerals and recycling, and global energy prices. Any EU decision on import tariffs is a flashpoint; approved tariffs may curb Chinese imports temporarily while accelerating Chinese investment in EU plants.

Strategic Implications

For European OEMs, the decision is whether to accelerate EV-factory capital expenditure and vertical integration or to deepen partnerships; cost competitiveness is decisive, and lower-cost battery chemistries such as LFP are central. For suppliers, the priority is targeting new gigafactories and EV lines, with battery-technology IP offering leverage and others needing consolidation. For investors, both European and Chinese capital see opportunity, though financing and timeline risk stays high. For policymakers, balancing trade and industrial policy is critical, with import volumes and OEM investment commitments the data points to watch. For consumers, more local EV models should widen choice, while protectionist measures that raise prices may slow uptake; charging infrastructure for trucks and buses will further shape adoption.

Conclusion

Europe's answer to China's low-cost EV challenge cannot rest on sales incentives alone; it requires rebuilding an end-to-end industry. EU policy and investment are spurring new factories, yet value capture depends on localizing batteries, cells, and materials. The next several years will determine whether Made in Europe becomes more than a slogan.